Tennessee Debt Relief by the Numbers: 5-Year Debt Trends

Although the cost of living in Tennessee is about 10.1% lower than the national average, many people in the state are struggling with debt.

Tennessee households had a median income of about $72,000 in 2024. And the average person in Tennessee owed about $54,700 in debt as of 2024, according to the Center for Macroeconomic Data. In comparison, the average debt on a national level in 2024 was $62,000.

If you're juggling a large amount of debt in Tennessee, it can easily become overwhelming. And if that’s happened to you, you're not alone.

Data from Freedom Debt Relief shows that many people in Tennessee are having a hard time managing debt. Among debt relief seekers, the average FICO Score in Tennessee was 585 as of June 2025, up from 575 in 2024.

Debt relief seekers in Tennessee had an average debt-to-income (DTI) ratio of 35% in 2024. As of June 2025, that number had risen to 38.4%. On a national scale, debt relief seekers had a DTI of 42.3% at that time, so Tennessee is a bit ahead of the curve. But even so, many people in the state may be having a hard time keeping up with debt, especially as costs continue to rise.

Tennesseans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

5-Year Debt Trends in Tennessee

Factors like inflation and tariffs have squeezed Americans’ paychecks in recent years, forcing them to take on more debt or fall behind on existing debt. And Tennessee is no exception. Between 2020 and June 2025, debt relief seekers in Tennessee saw their debt increase by about 33%.

The average minimum monthly debt payment among debt relief seekers rose from $1,390 in 2020 to $1,599 in mid-2025. Just as notably, credit card utilization for that group increased from 67.6% in 2020 to 75.1% in June 2025. Credit utilization shows how much of someone’s total credit is being used at once.

Higher credit utilization can lead to more past-due accounts, since larger amounts of debt can be harder to keep up with. The amount of past-due credit card debt among debt relief seekers rose from $4,488 in 2020 to $4,944 in June 2025—a 11.5% increase.

And it’s not just credit card debt that’s plaguing debt relief seekers in Tennessee. Between 2020 and mid-2025, unsecured debt among debt relief seekers in Tennessee rose from $71,165 to $77,179. Secured debt increased from $187,737 in 2020 to $242,795 in the same period. And total debt (secured plus unsecured) rose from $258,901 in 2020 to $319,974 in June 2025.

As of mid-2025, debt levels in Tennessee were rising with income level. Lower-income residents seeking debt relief had an average debt of $17,201, while those with high incomes had an average debt of $140,632.

Meanwhile, among Tennessee debt seekers in June 2025, borrowers with good and fair credit had more debt than borrowers with low, very good, and excellent credit. At the same time, debt relief seekers in Tennessee ages 36 to 50 had the most debt, followed by those ages 51 to 65.

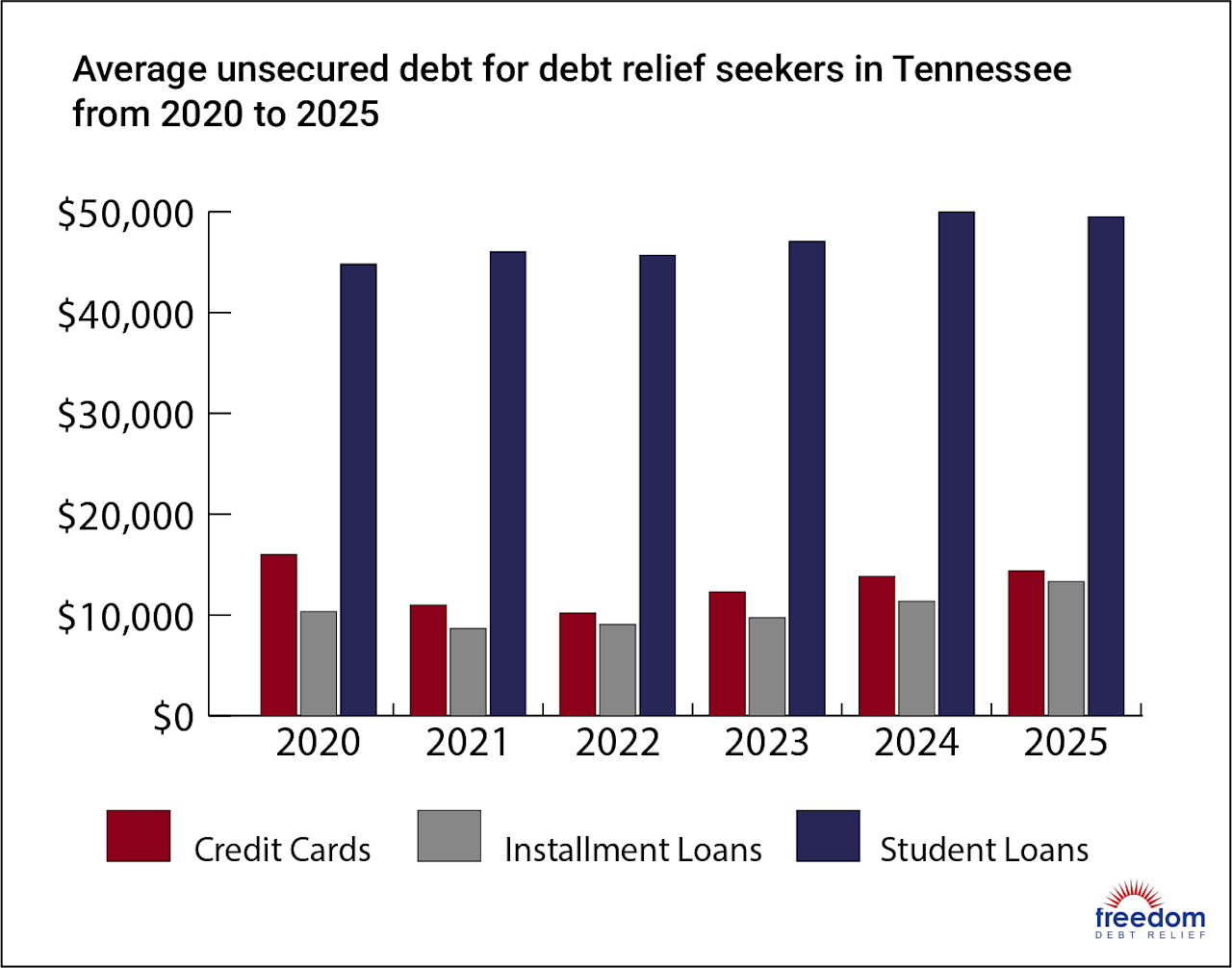

Tennessee credit card debt

Among debt relief seekers, average credit card balances actually dropped a bit from $16,014 in 2020 to $14,370 in June 2025. That's slightly lower than the national average credit card balance of $16,244 among debt relief seekers at that time.

The average monthly credit card payment held fairly steady for people looking for debt relief. In 2020, it was $452, and it fell to $449 in mid-2025. The average monthly payment actually dipped to $445 in 2024, a bit below the average monthly $489 credit card payment among debt relief seekers nationally as of June 2025.

However, credit card utilization rose from 67.6% in 2020 to 75.1% in June 2025 among debt relief seekers in Tennessee, just above the national average of 73.50% among debt relief seekers.

The average number of open credit card accounts held by debt relief seekers in the state declined from 7.7 to 6.9 during that same five-year period. That's a bit below the national mid-2025 average of 7.4 among debt relief seekers.

Credit card debt can be extremely challenging to pay off because credit cards tend to come with very high interest rates. Credit card interest can also compound frequently, making it easy for that interest to rack up against you. If you’re struggling with credit card debt, it could pay to seek credit card debt relief.

Tennessee auto loan debt

Among debt relief seekers, the average auto loan balance in Tennessee rose from $23,339 in 2020 to $27,736 in June 2025. That's just a bit higher than the average auto loan balance of $26,997 among debt relief seekers nationally at that time.

Meanwhile, the average monthly auto loan payment among debt relief seekers in Tennessee rose from $576 to $746, marking a percentage change of 29.5%. Despite that increase, that $746 payment is consistent with the average monthly auto loan payment of $749 across debt relief seekers nationally as of mid-2025.

Tennessee mortgage debt

Among debt relief seekers, the average mortgage balance in Tennessee rose from $164,398 in 2020 to $215,059 in June 2025. That’s a bit below the average mortgage balance of $239,406 among debt relief seekers nationally at that time.

The average monthly mortgage payment among debt relief seekers in Tennessee increased from $1,168 in 2020 to $1,668 in June 2025. Mortgage rates have risen substantially since 2020, so this is not so surprising. On a national scale, debt relief seekers had an average mortgage payment of $1,989 in June 2025.

Tennessee installment loan debt

Among debt relief seekers in Tennessee, the average installment loan balance rose from $10,340 in 2020 to $13,306 in mid-2025, marking an almost 29% increase. This is a notch lower than the average installment loan balance among national debt relief seekers of $12,632 in June 2025.

The average monthly installment loan payment for Tennessee debt relief seekers, meanwhile, rose from $363in 2020 to $446 in June 2025, a bit lower than the average monthly installment loan payment among national debt relief seekers, which is $485 as of that date.

Although installment loans can have lower interest rates than credit cards, sometimes those rates can also be high, depending on your credit score at the time of the loan.

Tennessee student loan debt

Among debt relief seekers, the average student loan balance in Tennessee rose from $44,811 in 2020 to $49,503 in June 2025. That's a tiny bit lower than the average student loan balance among U.S. debt relief seekers in mid-2025, which was $49,932.

Tennessee debt relief seekers had an average monthly student loan payment of $228 in 2020. The monthly average payment rose to $296 as of June 2025, when it was $313 nationally among debt relief seekers

If you owe federal student loan balances you're struggling to pay, there may be some protections available. These could include forbearance, deferment, or a new repayment plan.

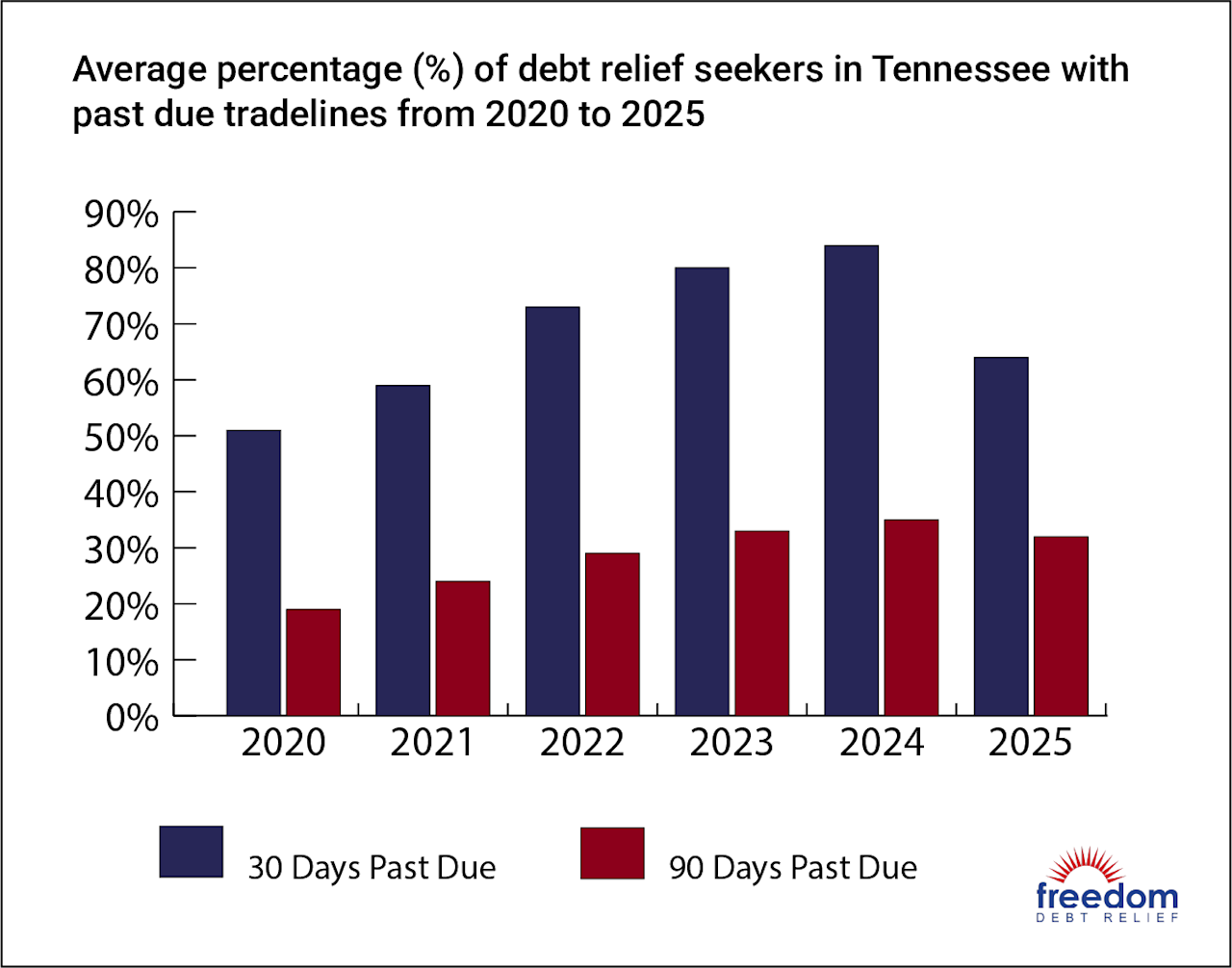

Tennessee Debt Delinquencies and Collections

Among debt relief seekers in Tennessee, there were 4.3 accounts in collections on average in 2020, compared to 2.2 in June 2025. The average balance in collections also fell from $3,880 in 2020 to $3,269 in June 2025. Among debt seekers nationally, the average collections balance was $3,040 as of that date.

Past-due collection amounts among Tennessee debt relief seekers, meanwhile, fell from $3,727 in 2020 to $3,000 in June 2025. On a national level, debt relief seekers also saw their collection past-due amounts fall over that period, from $3,694 to $2,884.

TransUnion has data on delinquencies across all residents of Tennessee—not just debt relief seekers. Here’s a summary of how Tennesseans are managing their debt.

| Type of debt | 30-plus days past due | 60-plus days past due | 90-plus days past due |

|---|---|---|---|

| Auto loan | 4.31% of consumers | 1.66% of consumers | Data not available |

| Credit card | 4.95% of consumers | 3.50% of consumers | 2.53% of consumers |

| Mortgage | 2.84% of consumers | 1.27% of consumers | 0.75% of consumers |

The longer a debt is past due, the more impact it can have on your credit score. And in the context of secured debts like mortgages and auto loans, past-due accounts can be problematic, because they can lead to foreclosure and vehicle repossession.

Tennessee Statute of Limitations

A statute of limitations is the amount of time a creditor can expect to successfully sue you to collect an unpaid debt. They may sue you after that point, but the debt is then considered “time-barred,” and therefore uncollectible. Here’s an overview.

| Type of debt | Tennessee statute of limitations |

|---|---|

| Credit cards | 6 years |

| Medical debt | 6 years |

| Personal loans | 6 years |

| Auto loans | 6 years |

| Mortgage lien | 10 years |

Generally, the statute of limitations clock starts on the date of your last payment. For installment loans like personal or auto loans, the clock starts on the date your payment is due. Note: If you make any payment toward a debt that’s beyond the statute of limitations, it resets the clock, making it collectible again.

What are the Tennessee debt collection laws?

Tennessee doesn’t have a specific debt collection law, though it has a statute of limitations on debt collection. However, it has the Tennessee Consumer Protection Act (TCPA), which generally protects Tennesseans against misconduct by creditors and debt collectors.

The TCPA works in conjunction with the Fair Debt Collection Practices Act (FDCPA), a set of federal laws designed to protect Americans from abusive or deceptive behavior in debt collections. The FDCPA bars debt collectors from calling at unreasonable hours, using inappropriate language, and making baseless threats against consumers.

Reviews and Testimonials from Tennessee

Great customer service always kind. All my answers were answered by customer service and a courteous way. Made feel important.

Joyce Rawn, US

Good job. Did it fast kept in touch

Steven Cain, US

Everything takes time-when the negotiations are visible-it’s a job well done.

Maria S, US

Tennessee Debt Relief

If you have overwhelming debt, a debt relief program could be a good way to deal with it. With these programs, a debt settlement company negotiates with creditors on your behalf. The goal is to convince your creditor to accept less than you owe and forgive the rest.

You typically make a monthly payment into a dedicated account (that you own and control). That money is used to repay your debts once there’s an agreement and you’ve greenlighted it.

A debt relief program is typically suitable for people who are far behind on their debts and don't have a path to paying off those debts in full. A debt relief program can take as little as two to four years to complete.

If you want to learn more about your debt relief options in Tennessee, contact Freedom Debt Relief to request a consultation. A debt consultant can speak to you about your financial situation, then work with you on a debt relief plan.

Is Debt Consolidation the Best Debt Solution?

If you’re struggling with debt but aren’t missing payments, debt consolidation may be the right choice. Debt consolidation is when you take out a new loan and use it to pay off other debt. It could make your debts easier to manage by lowering the number of monthly payments you have to make. Better yet, if you can lower the interest rate on your debt, you might find it more affordable.

If you have a lot of high-interest credit card debt, you may be able to lower your interest rate by paying if off with:

A personal loan

A 0% balance-transfer credit card

A home equity loan or line of credit (HELOC)

Debt consolidation could make the most sense if you:

Have a strong enough credit score to qualify for a debt consolidation loan or balance transfer credit card

Have planned ahead, and know you can pay off the new debt

Other Debt Relief Alternatives in Tennessee

Here are some other debt relief options that may be all or part of the solution for your situation:

Debt settlement. A debt relief company can negotiate with creditors on your behalf (or you can negotiate for yourself). Debt settlement seeks to reduce the amount of total debt you owe.

Hardship programs. These are arrangements some creditors offer to make it easier to pay what you owe. They may include delaying or reducing monthly payments, suspending late fees, or lowering your interest rate.

Income-driven repayment plans. These are most commonly offered in connection with government-backed student loans. These plans base your monthly payment on the amount of money you make. This can help you afford student loan payments on a lower income.

Credit counseling. Credit counseling can mean different kinds of help. It may simply entail having a qualified credit counselor explain your various debt relief options. Or it may involve a debt management plan. This is an ongoing relationship in which the credit counselor can manage your debt payments for you.

DIY debt payoff. You can pay off your own debts at your own pace by setting a budget and allocating money to your debt every month. Common strategies for this include the avalanche method, in which you pay off your debts from highest interest rate to smallest, or the snowball method, in which you pay off your debts from smallest balance to largest.

Bankruptcy. This is a legal solution. A court decides how to use your income or assets to settle your debts to the extent possible. If no other debt relief solution seems as if it will work, bankruptcy could get debt collectors off your back so you can start over.

Tennesseans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

What are the primary types of debt relief options available to Tennessee residents?

In Tennessee, there are a number of debt relief options available to people struggling to pay their debts. You could look at debt consolidation—moving your various debts into a single loan with a fixed monthly payment. You could consolidate any debts, but it’s usually only a good idea if your new loan has a lower interest rate than the debts you want to consolidate.

Another option is a debt management plan (DMP), which you arrange through a credit counseling agency. A DMP is a structured repayment program that, like a debt consolidation loan, gives you one monthly payment. Not all debts are eligible for a DMP.

If your debt just isn't payable, you may be able to negotiate a debt settlement agreement, on your own or with the help of a debt relief company. With debt settlement, your creditors agree to accept a lower amount than the sum you owe. While debt settlement could help you dig your way out of debt, it could also have a negative impact on your credit score.

Finally, if you qualify, Chapter 7 bankruptcy could be a way to walk away from all or most of your unsecured debts.

How does Chapter 7 bankruptcy work in Tennessee, including eligibility requirements?

A Chapter 7 bankruptcy is the liquidation bankruptcy—a court-appointed trustee sells certain assets of yours to pay your creditors as much as possible of what they are owed, and the rest of your qualifying debts are forgiven.

To qualify for a Chapter 7 bankruptcy in Tennessee, you must meet certain criteria. First, you must undergo credit counseling from an approved agency. You also need to pass a means test. The court wants to know if you have the means to repay your debts. If your income is below the Tennessee median, you generally qualify for Chapter 7.

The more people in your household, the more you can earn and still qualify to file for Chapter 7. For bankruptcy cases filed in Tennessee on or after November 1, 2025, the income limit to qualify for Chapter 7 is $62,339 for a one-person household, $80,722 for a two-person household, $95,011 for a three-person household, $106,775 for a four-person household, or $117,875 for a five-person household. (The numbers continue increasing for larger households.)

What are the benefits and drawbacks of a debt management plan in Tennessee?

A debt management plan (DMP) can be a good way to get rid of your debt. The credit counseling agencies that offer these plans can often negotiate reduced interest rates with your creditors, making your debts more affordable. With a debt management plan, you only have one monthly payment toward multiple debts. That could make your debt easier to manage and fit into your budget. And it could alleviate a lot of stress.

On the flipside, not all debts are eligible for a DMP. Typically, DMPs work with unsecured debts like personal loans and credit cards. They generally don’t help with mortgage debt, auto loans, or student loans.

A DMP usually requires you to close all of the accounts included in the plan. That could lower your credit score. There can also be fees involved with setting up a DMP, as well as ongoing service fees.

Are there specific Tennessee laws governing debt settlement companies and practices?

Tennessee's Uniform Debt-Management Services Act regulates companies that offer debt settlement services. Under this set of rules, debt settlement companies must register with the state before working with clients. Debt settlement companies must also disclose their fees before entering into any agreements, as well as explain the risks of debt settlement.

Debt settlement companies in Tennessee may not settle debts for more than 50% of the balance without the client agreeing. Debt settlement companies also can't offer a reward or compensation for referring a prospective client if the person or entity making the referral has a financial interest in the outcome of the debt.

There are also rules in Tennessee regarding how much debt adjustors or settlement companies can charge for their services. Debt settlement companies cannot charge more than $75 for an initial consultation. They also can't charge more than $50 per year in ongoing fees. At Freedom Debt Relief, the initial consultation is free. There are no ongoing fees for debt settlement services.

How does debt consolidation affect credit scores for individuals in Tennessee?

Consolidating your debt could improve your credit score. If consolidating helps you avoid late payments, and you make your new loan payments on time every month, you could establish a positive payment history. That’s the most important factor in credit scores.

Also, a debt consolidation loan might allow you to lower your credit utilization ratio, which measures how much of your available revolving credit you're using. The lower your utilization, the more your score might improve.

However, debt consolidation could also hurt your credit score. If you’re late on payments or skip them, that could damage your credit profile.

When you apply for a new loan, it leads to a “hard inquiry” on your credit report, which could drop your score by a few points. If a debt consolidation loan makes your debt more manageable so you don’t miss payments, that benefit could outweigh the relatively small drop in your credit score that typically comes from a hard inquiry.

Where can I find reputable non-profit credit counseling agencies in Tennessee?

If you’re looking for a reputable credit counseling agency in Tennessee, the National Foundation for Credit Counseling (NFCC) could help. You can use the NFCC's website to find a certified counselor in your area.

The U.S. Department of Justice also has a list of approved credit counseling agencies. You can use its website to find your judicial district by state and county.

The Consumer Credit Counseling Service of Chattanooga and the Tennessee River Valley is another good resource in Tennessee. Additionally, the Nashville Financial Empowerment Center offers free one-on-one financial counseling to residents of the Greater Nashville region.

Check a nonprofit credit counseling agency's rating on the Better Business Bureau to read up on consumer complaints and reviews. You can also check with your state attorney general to see if a credit counseling agency is legitimate.

While many reputable credit counseling agencies offer a free initial consultation, there are usually fees for their debt management plans. Agencies should provide all of that information from the start.

What are the income limits for Chapter 13 bankruptcy in Tennessee as of October 2025?

There are no fixed income limits to qualify for Chapter 13 bankruptcy in Tennessee. Unlike Chapter 7, where eligibility is based on a means test, with Chapter 13, you show proof of regular income to qualify. That’s because a Chapter 13 bankruptcy reorganizes your debts, and you repay them as part of a court-approved plan. Having a higher income doesn't necessarily disqualify you from filing for Chapter 13. However, your income helps determine your repayment plan.

Under a Chapter 13 bankruptcy, if your income is less than the median in your state, you generally have a three-year repayment period. If your income is higher than the median in your state, you usually have a five-year repayment plan.

While there generally are not income limits for Chapter 13 bankruptcy in Tennessee, there are debt limits. Those are the same nationwide, and are $526,700 for unsecured debts and $1,580,125 for secured debts.

What is the statute of limitations on debt collection in Tennessee?

The statute of limitations for medical debt and credit card debt in Tennessee is six years. That same six-year statute of limitations also applies to oral and written contracts.

Generally, the statute of limitations clock starts on the date of your last payment. For installment loans like personal loans, the clock starts on the date your payment is due.

Note: Making a partial payment, or even acknowledging a debt in writing or verbally, could reset the clock on the statute of limitations. That could give a creditor more time to successfully sue you for an unpaid debt.

Some debt collectors use sneaky tactics to reset the statute of limitations clock. Be very careful when talking to debt collectors about an older debt.

Are there free legal aid services for debt relief available to low-income residents in Tennessee?

Legal Aid of East Tennessee offers free civil legal representation in matters related to protecting your finances and identity. They can assist with issues such as bankruptcy, bill collections, foreclosure, and wage garnishment.

West Tennessee Legal Services also offers free legal aid. This includes advice and representation regarding debt collection lawsuits, harassment from debt collectors, credit counseling services, wage garnishment, and student loan collections.

Finally, the Debt Relief Clinic is a virtual clinic for Tennessee residents earning up to 200% of the Federal Poverty Level. The clinic helps people understand bankruptcy, and offers advice on whether it's a good option. The clinic also offers free or reduced-fee representation for Tennesseans who file for bankruptcy.

Have there been any significant changes to Tennessee debt relief laws or consumer protections in 2024-2025?

In May 2024, Tennessee passed Senate Bill 2375. Under this law, a creditor suing someone over a debt must present sufficient documentation to prove that the debt is valid before being awarded a judgment.

In April of 2025, Tennessee enacted the Debt Resolution Services Act. Among other things, it requires people or companies that provide debt resolution services to obtain a license. It also outlines rules for debt resolution services, including how to manage a dedicated account, and what information to disclose in consumer agreements.

Also, as of July 1, 2025, consumer reporting agencies in Tennessee are not allowed to include medical debt in credit reports. This includes medical debt reported to a collection agency, and judgments related to medical debt.

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months