Louisiana Debt Relief by the Numbers: 5-Year Debt Trends

American consumers have continued to sink further into debt since the COVID-19 pandemic ended. In Louisiana, many residents struggle to make ends meet on limited financial resources.

The rising cost of living affects all Americans. However, the burden falls more heavily on households in Louisiana, where annual incomes are about $12,000 lower than the U.S. average.

When people can't afford their expenses, they often borrow to make up the difference and borrowing sometimes gets out of hand. People in Louisiana are all too familiar with this pattern. The Pelican State has far more than the national average of borrowers who are 60 days or more overdue on payments for auto loans, credit cards, mortgages and personal loans.

Missing payments on debt could become a vicious cycle, when late payments mean more interest and also hurt credit scores. Across the U.S., the average FICO Score is 713, decreased since 2024 because of higher utilization and delinquency. In Louisiana, the average is a lot lower, at 687. That makes it more expensive to borrow. When people have to pay those higher interest rates on rising balances, maintaining debt costs more every month. Often, late fees pile on even more expense.

The solution is to break the cycle of debt before it goes too far. Tens of thousands of people in Louisiana seek debt relief every year. The first step is to find out about the available options, so you can decide what might work best for you.

Louisianians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

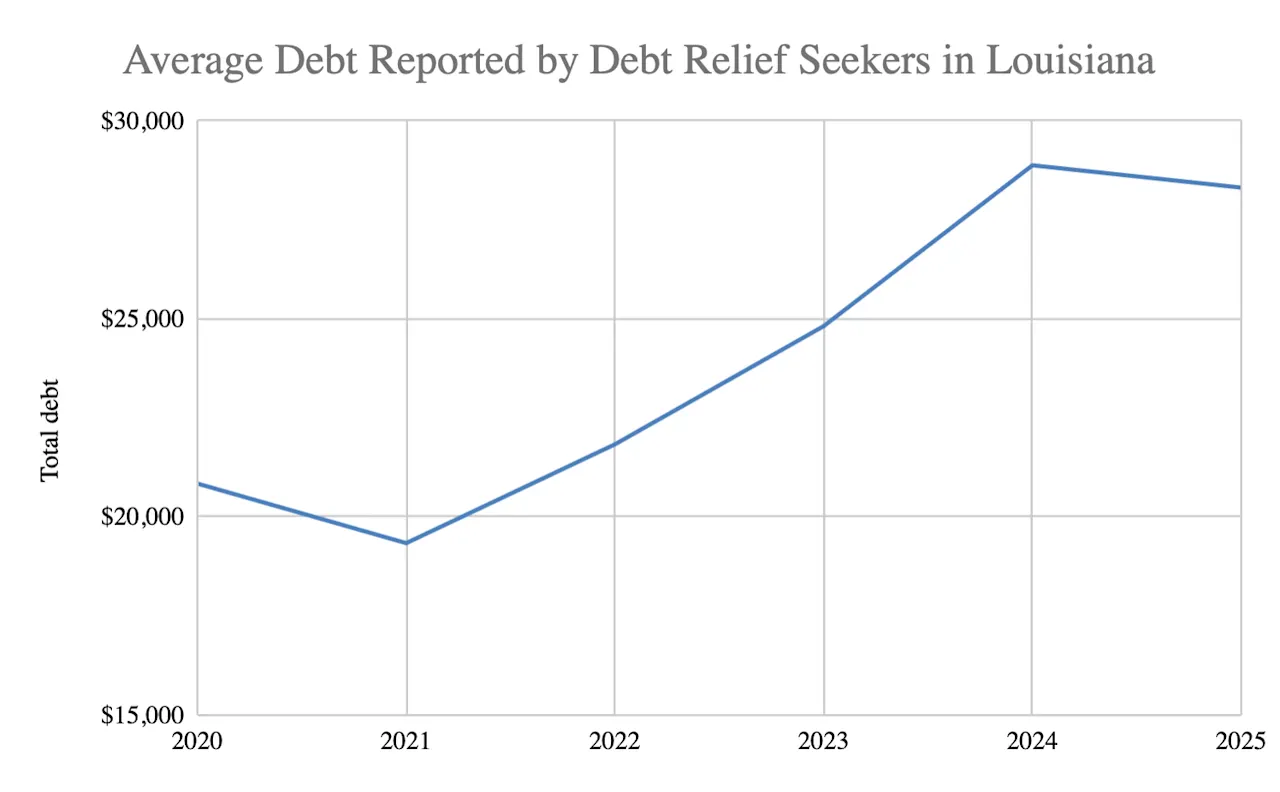

5-Year Debt Trends in Louisiana

Freedom Debt Relief has statistics on the financial condition of Louisiana residents who've inquired with us about debt relief over the past five years. These stats show how their average debt burden has risen over that time:

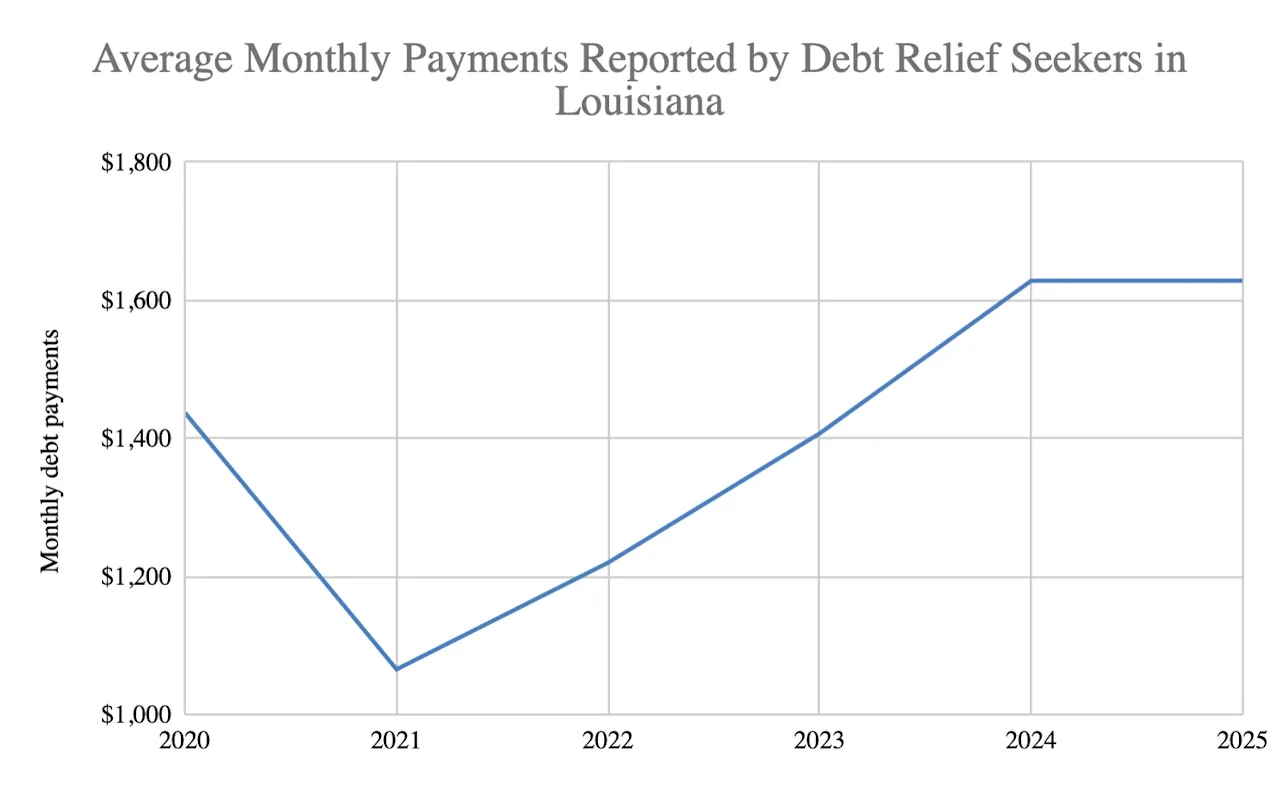

As the total amount owed has risen, so have the monthly payments on that debt:

Those monthly payments, which now average $1,628, are the knife point of the debt problem. Higher payments cut deeper into household budgets. This leads to more debt and higher monthly payments—and the cycle continues.

Here are other signs that debt has pushed some households in Louisiana close to the financial edge:

While average monthly payments have risen by 13.3% over the past five years, the average expected income of people seeking debt relief in Louisiana has dropped by 6.4%.

The average credit card utilization rate has risen during the same time from 67.4% to 75.7%. As people get closer to maxing out their credit cards, their financial options dwindle.

That 75.7% credit card utilization rate is above the national average.

While credit scores generally have risen over the past five years, for people seeking debt relief in Louisiana the average score has fallen by 17 points.

Average balances owed have risen for auto loans, personal loans, mortgages and student loans.

Debt problems in Louisiana peak as people approach retirement age. For most of the six years covered in our review, debt relief seekers between 51 and 65 owed more money and had higher debt-to-income (DTI) ratios than any other age group. Keeping up with this debt burden makes it harder to put money aside for retirement.

Different types of debt could create different problems. The nature of your debt problem depends on the type of debt you have. Here’s a closer look at different types of debt in Louisiana.

Louisiana credit card debt

Credit card debt has grown much heavier over the past three years. Over that time, those with credit card debt have seen balances increase by 40%—and more than a third of total balances are overdue. The average monthly payment has risen by 29%. As a result, they owe an average total credit card balance of $13,979. On average, over a third of this total is past due. Monthly minimum credit card payments now average $437.

Credit card debt is a particularly toxic type of debt. For one thing, it generally has higher interest rates than other conventional forms of consumer debt. The average interest rate on credit card debt is 22.83%. People with bad credit could pay about 10% more.

Another troublesome thing about credit card debt is that monthly minimum payments usually represent a very small percentage of the amount owed. Smaller payments make your debt last longer. As a result, you pay more interest. Also, people often charge more on their cards than they pay each month, so they see their debt rise over time instead of fall.

A silver lining to this is that most credit card debt is unsecured. That expands the field of credit card debt relief options, including debt settlement.

Louisiana auto loan debt

Kelley Blue Book recently reported that the average cost of a new car exceeded $50,000 for the first time ever. Not surprisingly, auto loans have become an increasingly heavy burden on debt relief seekers in Louisiana.

Those consumers with auto loans have an average balance of $30,250, up by 16.8% over the past five years. Even worse, average monthly payments on auto loans, at $828, are 27.1% higher than they were five years ago. Both those auto loan balance and monthly payment figures exceed the national averages for debt relief seekers.

Auto loans usually have fixed monthly payments, which should make them easy to plan for. However, debt relief seekers in Louisiana have higher payments with lower monthly incomes than the national averages, so it's not always so easy to make those payments.

That's a problem, because auto loans are secured by the vehicles they were used to purchase. If you can't make your payments, you may find yourself without transportation.

Louisiana mortgage debt

Debt relief seekers in Louisiana who have mortgages report owing an average of $173,126 on those loans. The average monthly payment is $1,606.

Both those figures are lower than the national averages. That sounds like good news until you consider that the median home value in Louisiana is nearly $150,000 lower than it is nationally. So, even with lower mortgage balances these homeowners don't necessarily have more equity.

The real problem is that mortgages have become a much bigger burden. People seeking debt relief in Louisiana who have mortgages have seen their average balance rise by 9.5% over the past five years. Worse, monthly payments have risen by 31.8%.

Since mortgages are secured by the properties they were used to buy, those soaring monthly payments can put some people's homes at risk.

Louisiana installment debt

Personal loans are a common form of installment debt. This debt represents an especially heavy burden on people seeking debt relief in Louisiana.

Consumers with this kind of debt reported an average balance of $14,009 in 2025. The average monthly payment on this debt is $501. Both those figures are higher than the national averages. With a lower average income in Louisiana, this debt takes a much larger bite out of household incomes in the state.

While some personal loans are secured by collateral, most are unsecured. This could create an opportunity for more debt relief options, such as debt settlement, for which only unsecured debt is eligible.

Louisiana student loan debt

Student loan payments were suspended during the pandemic. That allowed borrowers to put them on the back burner for a while. However, now that payment requirements have resumed, they've moved front and center among the debt problems for some households.

Debt relief seekers in Louisiana with student loans report an average balance of $48,795. That's close to the national average of $49,932. However, the average monthly payment in Louisiana is $348, which is considerably higher than the national average. Not only have payment requirements resumed, but that average monthly payment is 31.8% higher than it was five years ago.

Most student loan debt is in federal student loans, which are not eligible for certain kinds of debt relief, such as debt settlement. The federal government does offer debt relief solutions such as income-driven repayment and debt forgiveness under some circumstances. With average incomes in Louisiana below the national average, an income-driven repayment plan might be an especially good option.

Louisiana Debt Delinquencies and Collections

Debt comes in different forms for different people, and it's often a combination of debts that causes the problem.

Credit card debt is the most common type of debt among debt relief seekers in Louisiana—62.6% report having credit card debt, which is higher than the national average. With over a third of these credit card balances past due, credit card debt is often the debt type that leads to serious trouble.

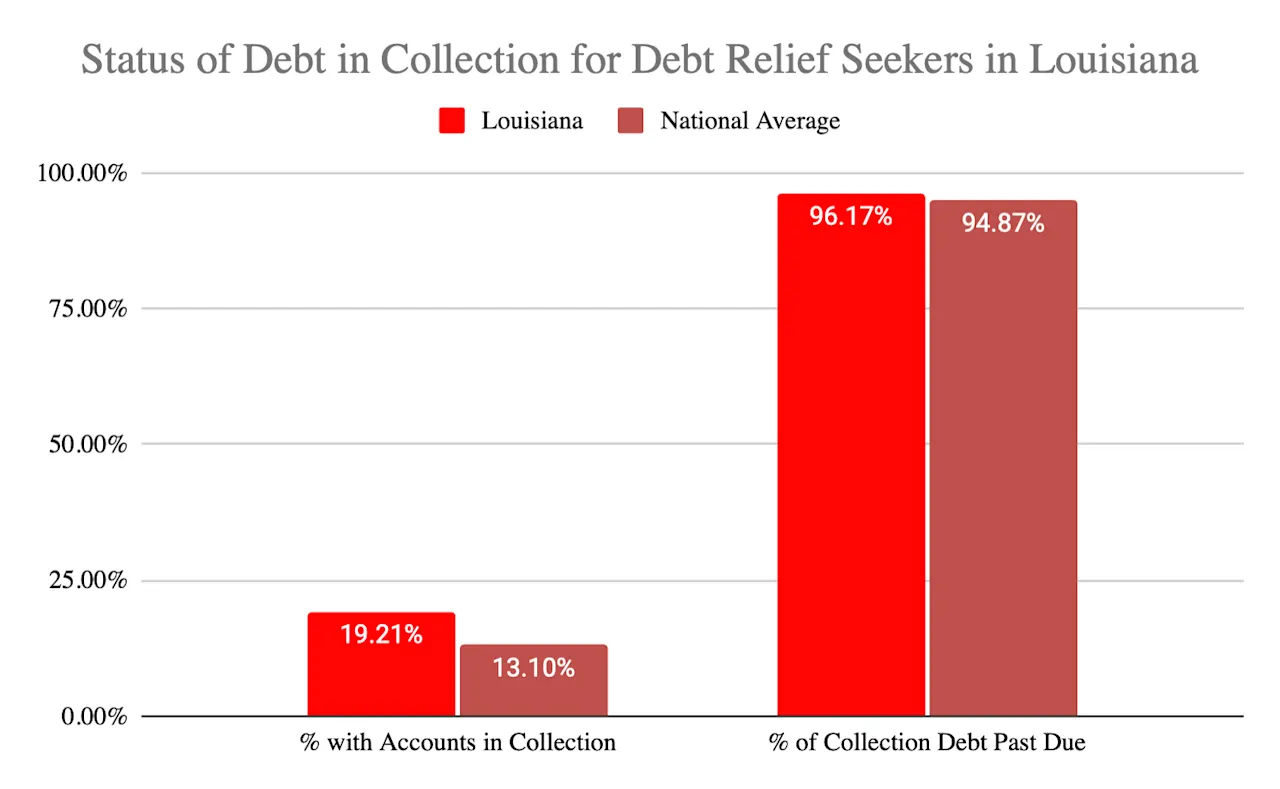

In Louisiana, 19.2% of people seeking debt relief have accounts that have been referred for collection. That's well above the national average of 13.1%.

These consumers have an average of 1.9 accounts in collection. The average amount in collection is $2,652. Of this, 96% of the total—$2,550—is past due.

As the chart below shows, for debt relief seekers in Louisiana the experience with accounts in collections is worse than the national averages:

The numbers show that people seeking debt relief in Louisiana are more likely to have accounts in collections than those nationally. They also have a higher percentage of their collection debt that’s past due.

By the time an account is referred to a collection agency, late payments have probably already damaged the borrower's credit score. Having accounts in collection is noted on credit reports, which is a warning sign to lenders.

On top of those problems with their credit records, borrowers with accounts in collection may have to fend off frequent contacts from debt collectors. This may prompt those borrowers to seek some form of debt relief. In many cases, they might be better off seeking relief before things reach that stage.

Besides looking into debt relief, once you have an account in collections it's important to know your legal protections.

Louisiana Statute of Limitations

A statute of limitations is a law that determines how much time a party has to take legal action against you. The length of time varies according to the type of legal action. Different states have different statutes of limitations.

In Louisiana, a creditor or collection agency has three years to sue you for nonpayment of credit card debt. The period for loans entered into by contract is 10 years.

Even after the statute of limitations has expired, a debt collector can still try to collect debt from you in other ways. That's why it's important to know what other legal protections you have, beyond the statute of limitations.

What are the Louisiana debt collection laws?

Debt collection activities fall under the Louisiana Unfair Trade Practice and Consumer Protection Act (LUTPCPA). This law broadly prohibits businesses, including debt collectors, from using unfair or deceptive trade practices.

Those violating this law are subject to enforcement by the state. The state may take legal action through the consumer protection divisions of the governor's or state attorney general's office. In addition, the law gives consumers the right to file a civil suit for damages under LUTPCPA.

LUTPCPA defines unfair and deceptive trade practices broadly, but actions of debt collectors are also more specifically limited under federal law. The federal Fair Debt Collection Practices Act (FDCPA) prohibits debt collectors from abusive, unfair, or deceptive acts.

Specifically, the FDCPA limits when, where and how a debt collector can contact you. It also requires them to provide written details on the debt they claim you owe and how you can contest it.

The information provided in this article is intended for general informational purposes only and should not be taken as legal advice. For personalized legal advice, consult with a qualified attorney licensed to practice law in your state.

Reviews and Testimonials from Louisiana

Celeste was very helpful and made sure I was clear on my next steps.

Annette Nelson, US

Very professional and courteous, he quickly took care of my reasons for calling. He was knowledgeable and helpful getting my questions answered.

Cindy Welschmeyer, US

Freedom Debt Relief made it easy to get credit card relief

Tim, US

Louisiana Debt Relief

You have several debt relief options. These can help you manage, reduce and in some cases even eliminate your debt.

One option you have if you're struggling to pay the bills is to see if you're eligible for various forms of public assistance available in Louisiana. You can find out about state programs from the Louisiana Department of Children and Family Services. In addition, you can find out about what federal assistance may be available from the U.S. Department of Health and Human Services.

While financial assistance may help you make ends meet, it won't directly help you with your debt. For that, you should consider a variety of debt relief options:

Organize your payments for maximum efficiency. Prioritizing debt payments with techniques such as the avalanche method could help you pay off your debts more cost-effectively.

Credit card hardship programs. Credit card companies usually won't publicize these. However, in some cases it's worth asking if they'll give you easier payment terms.

Debt management plans (DMPs). These are offered through non-profit credit counselors. You can find a list of credit counseling agencies approved to do business in Louisiana through the U.S. Department of Justice.

Debt consolidation. The key to this option is being able to qualify for less expensive credit to pay off high-interest debt

Debt settlement. This is a negotiation to reduce the amount you owe. You can do this yourself or get professional help from a debt relief company like Freedom Debt Relief.

Bankruptcy. Depending on your situation, you might be eligible for relief through a Chapter 7 or a Chapter 13 bankruptcy. You should ask a bankruptcy expert to explain your options.

Is Debt Consolidation the Best Debt Solution?

Debt consolidation and debt settlement are both common ways to handle debt. Which is better for you depends on your situation.

When you consolidate debt, you take out a new loan and use the money to pay off your credit cards, medical bills, or other debts. The new loan gives you just one loan payment each month. If the new loan has a lower interest rate than your current debts, you could get a lower monthly payment and/or save on overall interest charges.

Debt consolidation could make sense if you:

Have good enough credit to qualify for a cost-effective debt consolidation loan.

Want to simplify your monthly debt payments.

Owe an amount you believe you could handle with better payment terms. Debt consolidation doesn't reduce the amount you owe. It only combines your debts and allows you to change the terms like interest rates, minimum payments, and repayment period.

If you’re interested in debt consolidation, compare personal loans for debt relief from different lenders to estimate how much you could borrow and what you'd pay in interest. You could also consider a balance transfer credit card.

Debt settlement may be a good choice if you:

Can’t afford to fully repay your debts.

Have a financial hardship that makes it difficult to keep up with debt payments.

Owe mainly unsecured debt.

If you're looking for a debt relief firm to help you with debt settlement, consider the following:

Experience negotiating debt settlements in Louisiana. The laws involved with debt vary from state to state. Familiarity with local laws could impact the negotiation process.

Professional accreditations. Look for certification from organizations such as the Association for Consumer Debt Relief and the International Association of Professional Debt Arbitrators.

An extensive track record of success. Ask about how long the firm has been doing business, the number of people they've helped, and the results they've gotten.

Positive customer ratings on Google, Trustpilot, and Best Company.

No upfront debt settlement costs. A debt settlement company can’t charge you fees for settling debts until after they negotiate an agreement and at least one payment has been made towards it.

What's the typical situation for someone enrolled in a debt relief program in Louisiana? Freedom Debt Relief reports that as of 2025 its average client in Louisiana had $24,937 of unsecured debt enrolled in its program.

Getting more information could help you decide which is the right solution for your situation.

Louisianians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

How does Chapter 7 bankruptcy work in Louisiana?

Chapter 7 bankruptcy involves selling things you own to pay off part of your debt. To qualify, you must have a relatively low income.

The income limit is based on the median income in the state. In 2025, the limit for a single person household in Louisiana was $53,677. This limit is adjusted for the size of your household.

Chapter 7 bankruptcy in Louisiana can be resolved in a matter of months. While you may have to sell off many of your assets to pay off the debt, there are exemptions. These include:

Up to $35,000 worth of equity in your home.

Up to $7,500 worth of equity in a vehicle, plus another $7,500 for a vehicle fitted to accommodate a family member with a disability.

Up to $5,000 worth of personal property.

There are also a variety of more specific exemptions. You should check with a bankruptcy expert to see if these apply to you.

The court will supervise selling off the assets you’re not allowed to keep. Then, a bankruptcy judge will decide how to split the proceeds among your creditors. Once that's done, any remaining eligible debt will be erased. There are some debts that you can't get rid of through bankruptcy. These include taxes and other government debt, as well as spousal and child support.

Bankruptcy rules are complex and subject to change from time to time. Be sure to consult with an expert in your state before deciding whether bankruptcy makes sense for you.

How does a debt management plan affect credit score in Louisiana?

Signing up for a debt management plan (DMP) in Louisiana shouldn’t directly affect your credit score. However, some parts of that plan may have an impact.

Expect short-term negative credit impact if the DMP requires you to close credit card accounts. Reducing your available credit can immediately raise your credit utilization ratio. Also, closing older credit accounts may reduce the age of your credit.

On the other hand, the DMP could help you manage your finances, keep up with your payments, and build a positive payment history. Payment history is the biggest factor in credit scores.

As part of the DMP, some creditors may agree to update your payment status to current from past due.

In time, the positive impacts of a DMP could outlast negative ones. The key is to follow the plan and then avoid new debt going forward.

Are there nonprofit credit counseling services in Louisiana?

The U.S. Department of Justice has a list of nonprofit credit counselors in Louisiana. Some of the credit counselors on this list may be outside the state, but all are approved to provide services to Louisiana residents. Services may be provided in person, online, or by telephone.

A credit counselor may suggest a debt management plan (DMP). With a DMP, you send a single payment every month to the counseling agency. The credit counselor then makes sure the money is distributed to your creditors. There’s typically a modest monthly fee for the DMP.

A DMP doesn’t reduce what you owe. However, the credit counselor may get some creditors to agree to lower your interest rate and/or waive some fees.

Even if a credit counselor is part of a nonprofit and on an approved list, you should still check their qualifications and background to make sure they're right for your needs.

What are the pros and cons of filing Chapter 13 bankruptcy in Louisiana?

Chapter 13 bankruptcy requires you to agree to a payment plan over a three- to five year- period.

Here is a breakdown of some of the pros and cons of Chapter 13 bankruptcy in Louisiana:

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months