Pennsylvania Debt Relief By the Numbers: 5-Year Debt Trends

Many Pennsylvanians have significant debt. According to the Federal Reserve Bank of New York, the average resident had around $49,500 of debt in 2024.

Debt can quickly become overwhelming, especially if you have high-interest debt and can’t keep up with payments. Data from Freedom Debt Relief shows that many Pennsylvania residents have growing debt and are exploring debt relief options.

In 2024, Pennsylvania debt relief seekers had an average of $273,590 in total total debt. $73,891 of that was unsecured debt. The average monthly minimum debt payment was $1,517. Among Pennsylvania debt relief seekers, the average household income was $65,526.

Many residents have accumulated significant debt from credit cards, student loans, and installment loans. For those residents, debt relief solutions might be suitable.

Pennsylvanians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

5-Year Debt Trends in Pennsylvania

Over the last five years, debt has been a growing problem for many residents. Among Pennsylvanians seeking debt relief, total debt, which includes unsecured and secured debt, rose from an average of $236,685 in 2020 to $273,590 in 2024, a 15.59% increase.

Unsecured debt is debt that isn’t tied to anything valuable, such as credit cards and personal loans.

Still, the average Pennsylvanian seeking debt relief has less debt than the average U.S. debt relief seeker. Nationwide, debt seekers had average total debt of $288,638 in 2020, compared to $344,454 in 2025—a 19.34% increase.

The five-year average total debt for Pennsylvania debt relief seekers from 2020 to 2024 was $249,945. Of that, $67,573 was unsecured debt and $182,371 was secured debt. Secured debt includes mortgages and auto loans.

The average monthly auto loan payment and average monthly student loan payment have trended upward.

For debt relief seekers in the state, the average car loan payment went from $523 in 2020 to $66 in the first half of 2025. The five-year average payment from 2020 to 2024 was $579.

For Pennsylvania debt relief seekers, the average monthly student loan payment went from $258 in 2020 to $326 in the first half of 2025. The five-year average from 2020 to 2024 was $276.

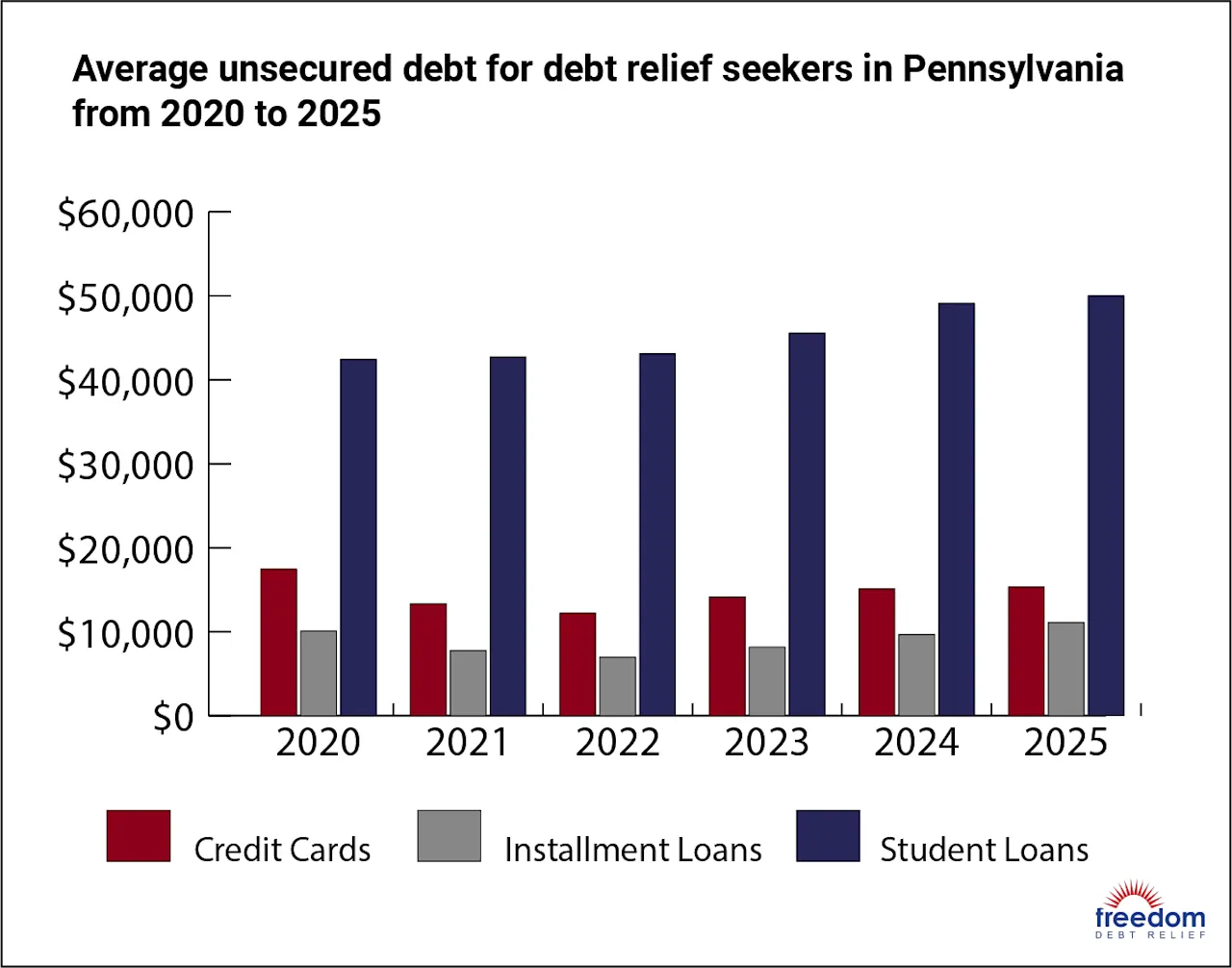

Pennsylvania credit card debt

Credit card debt is a growing problem for many debt relief seekers in the state. Since credit card debt is high-interest, unpaid balances can quickly spiral out of control, and debt can become unmanageable.

In 2024, the average credit card debt was $15,112 for Pennsylvania debt relief seekers. That’s close to the average of $15,636 for U.S. debt relief seekers.

Debt was spread across an average of 7.6 credit cards. The average past-due balance was $5,355, and the average monthly payment was $471.

That same year, Pennsylvanians seeking debt relief had an average credit utilization ratio of 75.8%. That means their credit card balances exceeded 75% of their credit limits. High utilization can be a sign of excessive debt that could benefit from a credit card debt relief program.

Pennsylvania auto loan debt

In 2024, debt relief seekers in Pennsylvania had an average monthly car payment of $645. The average car loan balance was $23,666. Both amounts have risen significantly in the last five years. In 2020, the average payment was $523, and the average balance was $19,310.

This is less than the national average. Among U.S. debt relief seekers, the average car payment was $726, and the average auto loan balance was $26,839 in 2024.

Around 43% of debt relief seekers in Pennsylvania have outstanding auto loan debt. The average number of open auto tradelines is 1.4.

Pennsylvania mortgage debt

Mortgage debt is a growing concern for many across the state.

Among Pennsylvania debt relief seekers in 2024, the average monthly mortgage payment was $1,516 and the average loan balance was $176,033.

This is significantly less than the national average for U.S. debt relief seekers. As a whole, debt relief seekers nationwide had an average monthly payment of $1,949 and an average mortgage balance of $241,535 in 2024.

Mortgage debt has grown throughout the last five years. In 2020, the average mortgage payment was $1,248. The average mortgage balance was $147,391. Meanwhile, in the first half of 2025, the average monthly payment was $1,591 and the average mortgage balance was $175,865.

Pennsylvania installment loan debt

Among debt relief seekers in the state, more than 30% have installment loan debt. This includes personal loan debt.

In 2024, the average Pennsylvanian debt relief seeker had $9,686 in installment loan debt. The average monthly payment was $377. Residents who seek debt relief have an average of 2.9 tradelines.

Pennsylvanians have slightly less installment loan debt than the average U.S. debt relief seeker. In 2024, debt relief seekers in the U.S. had $10,582 in outstanding installment loan debt. The average monthly payment was $436.

Unfortunately, this type of debt spiked in the first half of 2025. The average balance rose to $11,101 in Pennsylvania and $12,632 for debt relief seekers nationwide. Those seeking relief from their debt may be taking out larger personal loans.

Pennsylvania student loan debt

Nearly one in four Pennsylvanians seeking debt relief had outstanding student loan debt in 2024. Among them, the average monthly student loan payment was slightly higher in 2024 compared to that of U.S. debt relief seekers.

For Pennsylvanians seeking debt relief, the average student loan payment was $307 in 2024, compared to $298 for debt relief seekers nationwide.

Pennsylvania debt relief seekers carried an average of $49,092 in student loan balances in 2024, slightly less than the average loan balance of $49,861 for U.S. debt relief seekers.

Student loan debt has been trending upward. In the first half of 2025, the average payment in Pennsylvania was $326. The average student loan balance was $50,008.

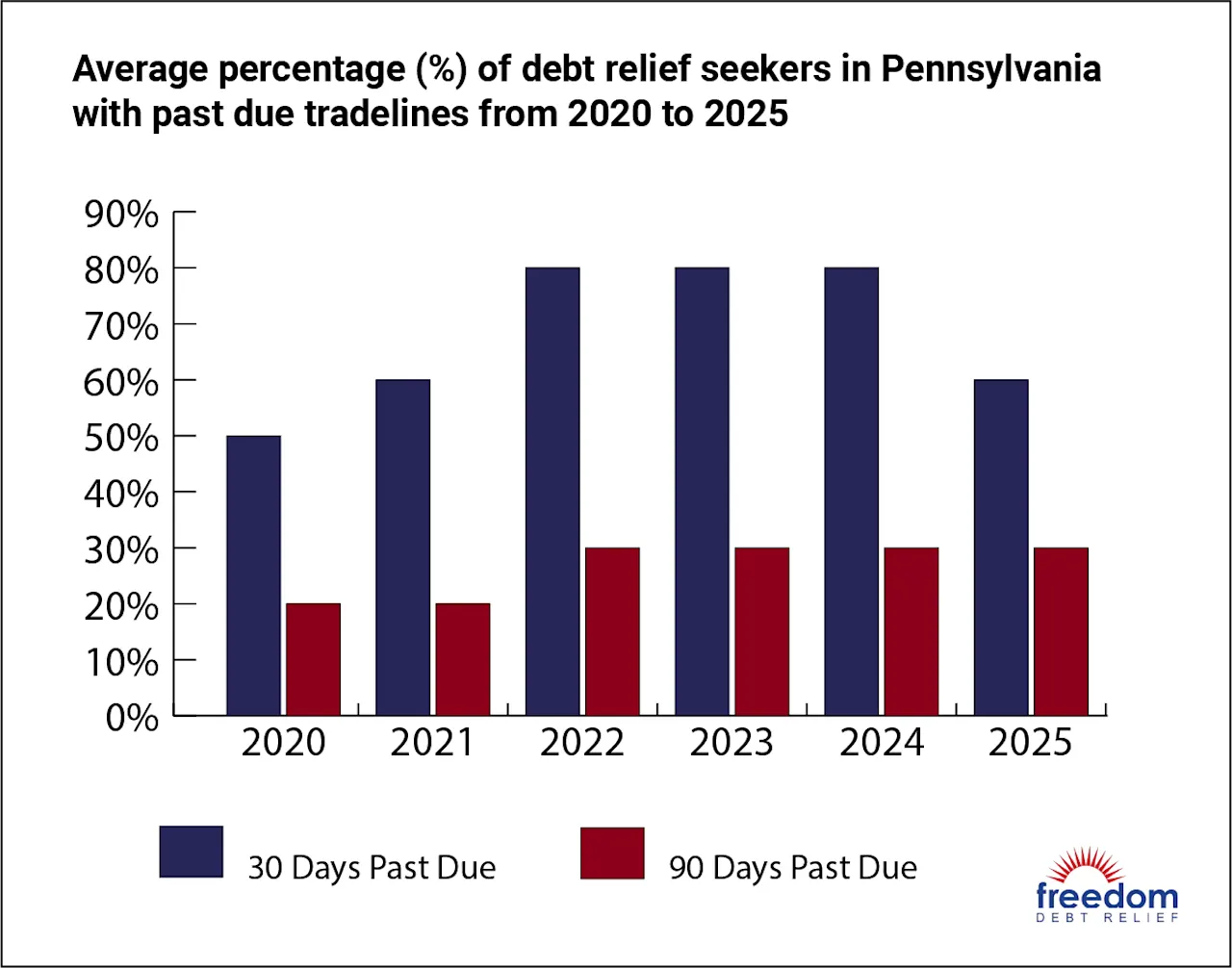

Pennsylvania Debt Delinquencies and Collections

TransUnion debt data from September 2025 shows that delinquency rates in Pennsylvania are above the national average for mortgages. 3.26% of mortgage accounts in Pennsylvania are at least 30 days past due (DPD), compared to the national average of 2.89% 30 days DPD.

Credit cards are the area where Pennsylvanians struggle the most, with 4.52% being at least 30 DPD. This is slightly below the national average of 4.66%.

This table outlines delinquency rates for Pennsylvania auto loans, credit cards, and mortgages, with the percentage that are at least 30, 60, and 90 days past due:

Delinquency Rates for Debts in Pennsylvania

| Type of debt | 30+ DPD | 60+ DPD | 90+ DPD |

|---|---|---|---|

| Auto loan | 4.0% | 1.51% | N/A |

| Credit card | 4.52% | 3.19% | 2.32% |

| Mortgage | 3.26% | 1.53% | 0.96% |

Based on Freedom Debt Relief debt data, the average balance for open collection agency tradelines among Pennsylvanians seeking debt relief was $2,431 in 2024. This is significantly lower than the average for debt relief seekers nationwide, which totaled $3,183 in 2024.

Among Pennsylvanians seeking debt relief, past due credit card debt averaged $5,355 in 2024. This is close to the national average of $5,240 for debt relief seekers that year.

Pennsylvania Statute of Limitations

In Pennsylvania, the statute of limitations for debt collection is typically four years. This time limit applies to most unsecured debts, including credit cards and medical bills.

Pennsylvania laws regarding statute of limitations on credit card debt

For credit card debt, the clock starts once you fail to make a payment on the due date. That means creditors don't have legal standing to sue you more than four years from the date your last payment was due.

Here's a breakdown of Pennsylvania's statute of limitations for various types of debt:

Pennsylvania Statute of Limitations for Debt

| Type of debt | Statute of limitations |

|---|---|

| Credit cards | 4 years |

| Medical bills | 4 years |

| Personal loans | 4 years |

| Auto loans | 4 years |

What are my rights against debt collector harassment in Pennsylvania?

Debt collection laws exist in Pennsylvania that can protect you from harassment. In Pennsylvania, the Fair Credit Extension Uniformity Act regulates debt collection practices. The law outlines actions that are considered unfair or deceptive. When attempting to collect debts from you, creditors and debt collectors must follow the law.

Creditors and debt collectors can't harass, oppress, or abuse you when attempting to collect debts. They can't threaten you with harm, use obscene language, or contact you by phone more than seven times within a seven-day period.

Unless you have given prior consent or the circumstances are allowed by the court, debt collectors may not communicate with you in the following ways:

Before 8 AM or after 9 PM

At unusual times or places

Using a specific method of communication after you have requested that they stop using that method

At your place of work, when your employer prohibits it

When they know an attorney represents you

Reviews and Testimonials from Pennsylvania

SO HAPPY that I decided to choose FDR, such a BIG load OFF my mind, knowing that this Company can be trusted to handle my Debts... SUCCESSFULLY! Thank you FDR...for calming my nerves, allowing me peace and tranquility 🙏🤗🥰

Jerri Puckett, US

Great experience, always helpful.

Daniel Herrera, US

Exelente company. They showing the advantages about my debit. Always send a email. And I can saw the results at any time. Thank you!

Maria Castaneda, US

Pennsylvania debt relief explained: real options, scams, & state laws

Pennsylvania Debt Relief

A debt relief program may make debt more manageable. These programs can provide a path to get rid of overwhelming debt.

Here's how it works: You make one monthly deposit into a dedicated debt settlement account (that you own and control), and a debt relief company negotiates with your creditors on your behalf.

Debt relief is an option for consumers who struggle to keep up with their debt payments and can't afford to repay their debts in full. A debt relief program can take as little as 24 to 48 months. A reputable debt relief company won’t charge you a debt settlement fee until they reach a deal with one of your creditors to settle one of your debts, you agree to the terms, and at least one payment is made toward the agreement.

In 2024, Freedom Debt Relief clients in Pennsylvania had an average enrolled debt of $24,226.

Want to learn more about Pennsylvania debt relief? Call Freedom Debt Relief to request a free, no-obligation debt consultation. A debt relief expert can explain your options and could create a custom debt relief plan that works with your income and expenses.

Is Debt Consolidation the Best Debt Solution?

There are no official state-run debt relief programs. But other debt relief solutions exist.

What are the main types of debt relief programs available to Pennsylvania residents?

Here are a few solutions Pennsylvanians struggling with debt can explore:

Debt settlement. Debt settlement involves negotiating with your creditors to accept less money than you owe. You can handle the negotiation yourself or work with an experienced debt settlement company.

Debt consolidation loan. You combine multiple debts into a single monthly payment with a new loan, ideally with a lower interest rate. A debt consolidation loan could streamline debt repayment.

Debt management plan (DMP). In a debt management plan, you pay off your unsecured debt in three to five years. DMPs are set up and managed by nonprofit credit counseling agencies. A DMP won’t reduce what you owe, but creditors might waive some fees or lower your interest rates.

DIY debt payoff. Another option is a DIY approach to debt payoff. Focus on paying off one debt at a time, and tighten your budget so you can put extra money toward your debt. Debt repayment strategies like the debt snowball method or the debt avalanche method may help you stay motivated.

Bankruptcy. Bankruptcy is a legal protection from creditors. If you’re eligible for Chapter 7, you could walk away from your unsecured debts. Chapter 13 is a three- to five-year repayment plan, with the potential for partial debt forgiveness at the end.

Compare debt settlement vs debt consolidation pros and cons in Pennsylvania

Debt settlement is also known as debt relief, and it means negotiating with your creditors to accept less than you owe but consider it payment in full. You can do this yourself or with the help of a professional debt relief company like Freedom Debt Relief.

Debt consolidation means getting a new loan and using it to repay multiple other debts. It’s a way to reorganize your debt and ideally make it easier to pay off. You’ll repay all that you owe.

Here’s how the two compare:

Debt settlement pros:

Resolve debt for less than you owe

Affordable monthly payments

Good credit is not required

You can DIY or hire a professional debt settlement company

Debt settlement cons:

Only works with unsecured debts, like credit cards and medical bills

You’ll have to save up settlement money over time

Pay fees to work with a company

Typically has a negative impact on credit

Debt consolidation pros:

You (hopefully) end up with fewer monthly payments

Could lower the interest rate on your debt

You get a set payoff date for your consolidated debt

Debt consolidation cons:

Typically requires good credit

Fees are typical for loans and balance transfer credit cards

Doesn’t reduce the amount you owe

Pennsylvanians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

Pennsylvania programs for homeowners struggling with mortgage payments

Help may be available if you're a Pennsylvania homeowner struggling to pay your mortgage.

The Homeowners' Emergency Mortgage Assistance Program (HEMAP) is a state-run program that helps homeowners avoid foreclosure. The program provides loans up to $60,000 to Pennsylvania homeowners at risk of foreclosure who are unable to make their mortgage payments due to circumstances beyond their control.

In repayment, you’ll have to pay between 35% and 40% of your net monthly income, as determined by HEMAP. Repayment is based on household income. The minimum monthly payment amount is $25.

Eligibility requirements for Pennsylvania government assistance programs for debt

Pennsylvania has no government assistance programs for debt relief. But financial assistance programs could provide support while you work to tackle your debt.

Here are some programs to consider:

LIHEAP (Low-Income Home Energy Assistance Program) provides cash assistance to help eligible low-income Pennsylvania families pay their heating bills. Applications are accepted from November to April.

SNAP (Supplemental Nutrition Assistance Program) is a federal program that provides eligible families with funds for groceries and nutritious food.

WIC (Women, Infants and Children) offers food packages tailored to the needs of women and children, along with nutrition counseling and breastfeeding support.

If you don’t meet the income qualifications for SNAP or WIC, local food pantries could be a resource. Feeding Pennsylvania has an online tool to help you find nearby food banks.

Are there specific debt relief options for medical bills in Pennsylvania?

Pennsylvania has no state-run medical bill debt relief programs. If you have a medical bill you can’t pay, income-based financial support programs from hospitals and healthcare systems may help. These programs could reduce the amount you owe, even if you've already received a bill.

How does Chapter 7 bankruptcy filing in Pennsylvania affect my assets?

When you file Chapter 7, you’ll give the court a list of everything you own.

Some assets are exempt, meaning you get to keep them. The court will sell your nonexempt assets and give the money to your creditors.

You must have lived in the state for at least two years to qualify for Pennsylvania state exemptions. You can choose either the federal or state exemption list, but you can’t combine them. Federal exemptions tend to be more generous than Pennsylvania's exemptions:

List of accredited non-profit credit counseling agencies in Philadelphia, PA

Are you a Philadelphia resident who wants to work with a credit counselor? Philadelphians have access to nonprofit credit counseling agencies. If you want to work with a nonprofit credit counselor, here's how to choose a reputable company.

The National Foundation for Credit Counseling (NFCC) can help you find Philadelphia credit counselors. The NFCC certifies member agencies to make sure they have the knowledge and skills to provide quality financial counseling.

Credit counseling agency members of the NFCC must meet the accreditation standards of the Council on Accreditation (COA). The COA is an independent nonprofit accrediting organization. All NFCC members must also follow NFCC's member quality standards.

To be connected with NFCC-approved credit counseling agencies in Philadelphia, call the NFCC at 1-800-388-2227, or fill out a form at nfcc.org/agency-finder.

If you live in or around Philadelphia, you might qualify for free financial counseling, available at Financial Empowerment Centers (FEC) in the city. You can schedule a free financial counseling session by calling 1-855-FIN-PHIL (855-346-7445).

How to identify and report debt relief scams in Pennsylvania

Many legitimate debt relief companies exist, but debt relief scams are on the rise. Here are some warnings signs of potential fraudulent debt settlement or debt negotiation services:

Asking for payment before providing services

Making guarantees about how much debt will be forgiven

Contacting you out of the blue

You can report debt relief scams to the Federal Trade Commission (FTC) at reportfraud.ftc.gov.

A state-run consumer protection hotline is also available for residents to report scams and other concerns. You can report financial, insurance, or consumer concerns at pa.gov/consumer, by calling 1-866-722-6675, or by sending an email to [email protected].

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months