California Debt Relief by the Numbers: 5-Year Debt Trends

California living comes with a steep price tag. Homes, for example, cost twice as much as they do elsewhere. It's not unusual for residents to have debt when life here is so expensive.

How much debt? On average, Californians have $87,570 in combined debt, according to the Center for Microeconomic Data. That includes mortgage debt, auto loans, student loans, and credit cards. The typical American, by comparison, owes $63,340. Among Californians seeking help from Freedom Debt Relief, the average debt as of June 2025 was $30,929.

What did the typical California debt relief seeker look like as of mid-2025? Here's a quick snapshot:

The average FICO Score was 598 (for perspective, a "good" credit score is 670 or higher).

Californian debt relief seekers paid $1,948 on average in minimum debt payments, and 43% of their gross income went to debt.

The average debt relief seeker had at least one account in collections and owed an average collection balance of $3,536.

If any of this sounds familiar, you might be a good candidate for California debt relief. Debt relief, or debt settlement, could help you pay off balances for less than what's owed. Debt settlement is regulated under the California Consumer Financial Protection Law to ensure that people who need help are protected from predatory practices.

Californians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

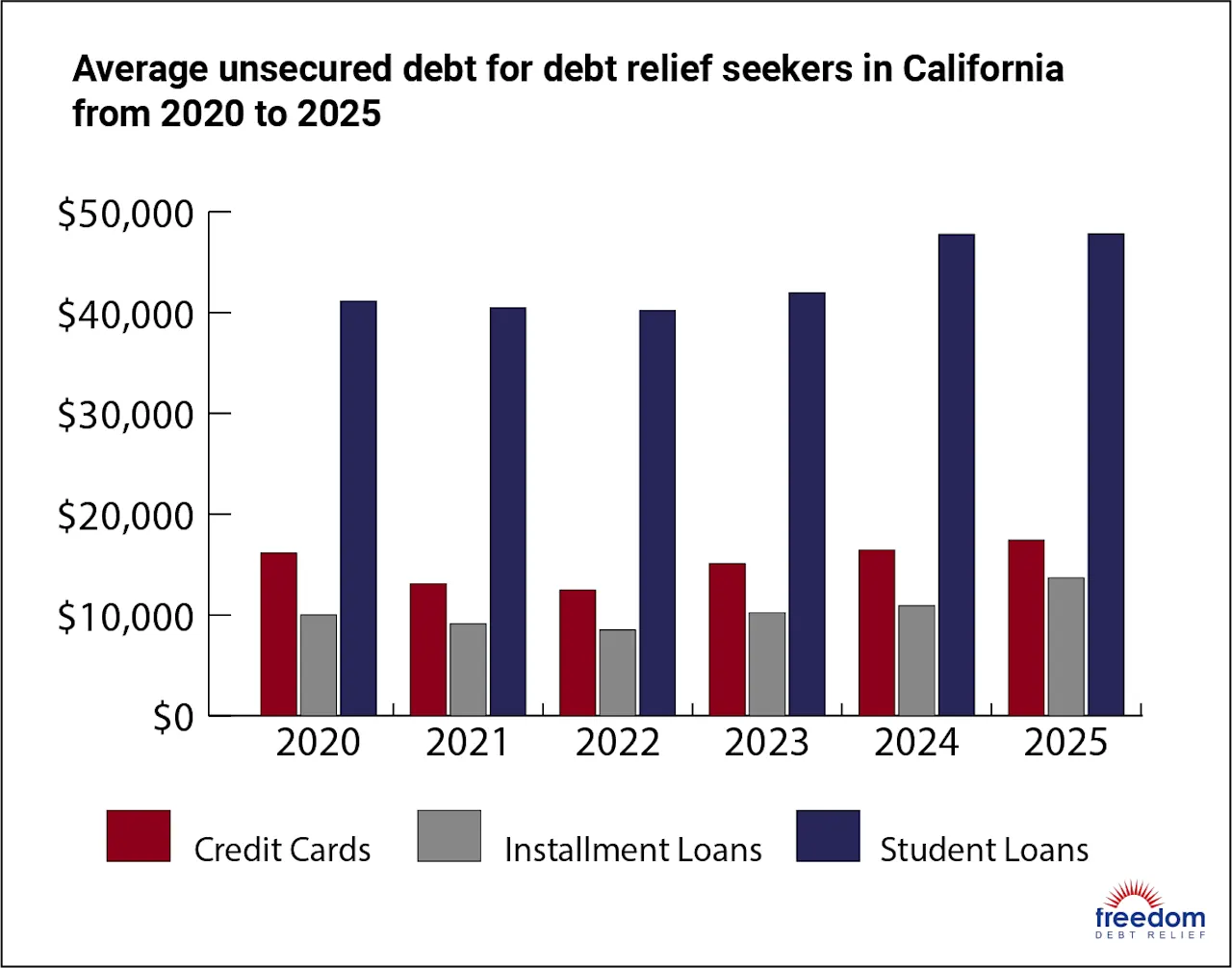

5-Year Debt Trends in California

From 2020 to mid-2025, debt levels in California dipped. That's a surprise, albeit a positive one, since debt levels nationwide rose on average over the same period. Here's how California debt levels have trended over the last few years:

These numbers represent the average amount of debt among people seeking debt relief. If you look at debt all together, including mortgage balances, student loans, credit cards, auto loans, and installment loans, the number shoots higher. According to Freedom Debt Relief's research, Californians owed an average of $508,312 as of June 2025. The bulk of that number is mortgage debt, with student loans making up the next biggest chunk. Still, it's well above the $345,211 Americans seeking debt relief owe on average.

Let's look at some additional five-year debt trends for Californian debt relief seekers:

Younger people rely most heavily on credit cards. Between 2020 and June 2025, the average credit utilization ranged from 77.2% at the low end to 90.3% at the high end.

High-income relief seekers consistently had the most debt overall between 2020 and June 2025. Conversely, debt levels were lowest among the lowest earners over that same period.

Credit card balances increased slightly, from an average of $16,150 in 2020 to $17,421 in mid-2025. Past due amounts, meanwhile, rose from $5,645 to $6,330.

Californians saw the percentage of their income allocated to debt jump from 31.5% in 2020 to 43.1% in June 2025.

On average, Californian debt relief seekers pay more toward debt per month and use more of their credit limit, despite an overall downward trend in debt levels. Interestingly, the average income was up from $69,588 in 2020 to $71,113 in June 2025. That could mean that even though residents bring home more money, they have to spend more to live, thanks to inflation.

California credit card debt

Credit cards, while convenient, can be difficult to pay off if you're stuck with high interest rates or can only afford to pay the minimums. The average person in California seeking debt relief:

Owes $17,421

Has 7.4 open credit card accounts

Pays $507 per month to their cards

Has a past-due card balance of $6,330

What about California credit card debt vs. the rest of the country? Nationwide, credit card users seeking debt relief carried an average balance of $16,244 across seven cards and paid an average $489 per month as of June 2025. Of that balance, $5,793 is past due. Credit utilization among California debt relief seekers was a slightly lower 72.2%, compared to 73.5% for the U.S. average among the same group.

Who owes the most debt in California by age? Here’s the breakdown of debt relief seekers in the state as of June 2025:

CA credit card debt by age group

| Age Group | Average Credit Card Debt | Average Total Debt |

|---|---|---|

| 18-25 | $9,922 | $23,416 |

| 26-35 | $13,606 | $24,753 |

| 36-50 | $18,367 | $33,007 |

| 51-65 | $18,719 | $31,501 |

| 65+ | $17,741 | $28,829 |

Credit card debt relief could help if you have balances you struggle to pay down. You can get rid of debt faster, reduce what you owe, and get your finances back on track.

California auto loan debt

Cars don't come cheap, and among California residents seeking debt relief who have an auto loan, the average balance is $26,949 as of June 2025. In 2020, the average was $21,089. Balances are highest for middle-aged people and lowest among seniors.

The average 36- to 50-year-old owes $29,508 in auto debt.

People 65-plus owe $22,138 on average.

Here's how California compares to the rest of the U.S. in seekers of debt relief

CA auto loan debt

| California Residents | U.S. Borrowers | |

|---|---|---|

| Total Balance | $26,949 | $26,697 |

| Monthly Payment | $765 | $749 |

| Average Number of Loans | 1.4 | 1.5 |

Debt relief can't get rid of a car loan you're still paying off, but it could help if you have a deficiency balance from a repossession. A repo can happen if you stop making your car payments.

Repossessed vehicles can be sold at auction. If the lender doesn't get enough money to cover the amount due on your loan, what's left is a deficiency balance. The lender can come after you to get you to pay that amount. California debt relief could help you negotiate the balance down.

California mortgage debt

Home ownership is never cheap, especially in California. Residents who have a mortgage owe $402,449 on average in mid-2025. The typical homeowner has just one loan, which suggests they may not be taking advantage of home equity loans or HELOCs.

Balances are highest for residents 26 to 35 seeking debt relief, which makes sense, since this is when many people buy a first home. They owe $426,544 on average. High-income earners owed the most to their mortgage overall in June 2025. They have a whopping $1.38 million in mortgage debt on average.

Here's how the state mortgage debt compares to the national average of debt-relief seekers.

CA mortgage debt

| California Residents | U.S. Borrowers | |

|---|---|---|

| Total Balance | $402,449 | $239,406 |

| Monthly Payment | $2,862 | $1,989 |

| Average Number of Loans | 1.2 | 1.2 |

For some context, the average home value was $761,003 as of November 2025. Nationwide, the average was $360,727.

California installment loan debt

Installment loans are repaid over time in set increments. For example, a personal loan might have a three-year repayment term. You pay the same amount every month until it's paid off.

The average Californian seeking debt relief has 2.8 installment loans and owes $13,675 as of June 2025. In 2020, they had 2.3 loans on average and owed $10,013. The upward shift could mean that more residents are relying on personal loans or lines of credit to meet their financial needs.

Here's how the numbers compare to debt-relief seekers nationwide.

CA installment loan debt

| California Residents | U.S. Borrowers | |

|---|---|---|

| Total Balance | $13,675 | $12,632 |

| Monthly Payment | $537 | $485 |

| Average Number of Loans | 2.8 | 2.8 |

Debt relief in California can extend to installment loans if they're unsecured. An unsecured loan isn't attached to any collateral, like a car or a home. If you have trouble with installment loan debt that you can't pay, debt relief could help.

California student loan debt

Between Stanford University, the California Institute of Technology, and the University of California network of schools, the Golden State has a thriving academic scene. That's an upside, but many colleges and universities here come with a high price tag.

Californians seeking debt relief owed $47,818 to student loans in mid-2025, with 4.4 loans on average. In 2020, they had 3.6 loans on average, and owed $41,155 instead. The jump could be attributed to rising tuition costs statewide and the need for more financial aid to cover the gap.

Seniors are carrying substantial student debt. In fact, people 65 and older owed the most student debt as of June 2025, at $58,176 on average. That's concerning, since loan payments could be a threat to their financial security in retirement.

Here's how California student loan debt stacks up against the national numbers for people seeking debt relief.

CA student loan debt

| California Residents | U.S. Borrowers | |

|---|---|---|

| Total Balance | $47,818 | $49,932 |

| Monthly Payment | $317 | $313 |

| Average Number of Loans | 4.4 | 5 |

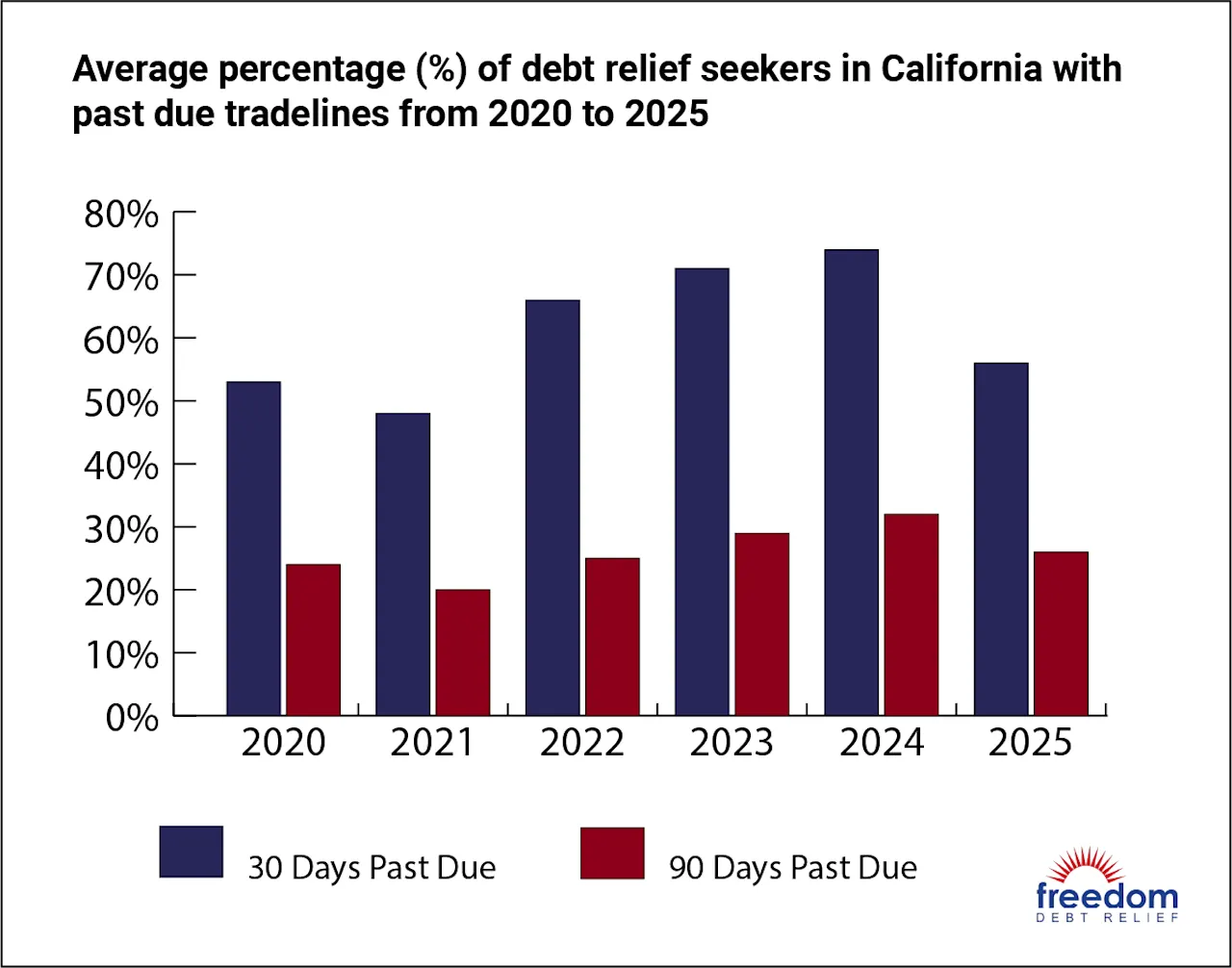

California Debt Delinquencies and Collections

When debts go unpaid those accounts could end up in collections. That's a problem, because a debt collector could try to sue to get you to pay. At the very least, you might have to deal with frequent phone calls or letters from a debt collector.

Californians looking for debt relief have fewer collections accounts than the average American seeking help for debt, but they owe more in collection debt. There’s one positive sign, however. Between 2020 and mid-2025, the average collection balance and average collection past-due balance both fell.

California debt relief could help with collections, though it doesn't guarantee that a lender won't sue you. If your creditors are willing to negotiate, however, debt settlement could help you pay off collection accounts for less than what's owed.

California Statute of Limitations

California generally has a four-year statute of limitations on debt that stems from a written contract. The statute of limitations determines how long a creditor has to sue you for a debt. They could still contact you about the debt if the lawsuit window closes.

The statute of limitations can vary for different debts. Here's how long the statute of limitations applies to each type of debt in California.

CA statute of limitations for debt

| Type of Debt | Statute of Limitations |

|---|---|

| Credit cards | 4 years |

| Medical debts | 4 years |

| Auto loans | 4 years |

| Private student loans | 4 or 6 years, depending on how the contract is classified |

| Mortgages | 4 years |

| Personal loans | 4 years |

| Judgments | 10 years |

| Oral contracts | 2 years |

| Promissory notes | 4 years |

| State tax debt | 20 years |

California debt relief could help with some of these debts, but not all. For example, you wouldn't be able to get help with mortgage or tax debt. If you're not sure which of your debts might be eligible for relief, a chat with a debt expert can give you clarity.

What are the California debt collection laws?

The Rosenthal Fair Debt Collection Practices Act protects Californians against unfair or abusive practices from debt collectors. Under the law, debt collectors must:

Only contact you between 8 a.m. and 9 p.m., unless you agree to let them contact you at other times

Contact your attorney if they're aware you have representation

Refrain from calling you at work if they're aware you can't get personal calls while on the job

Not harass or threaten you, or use abusive or profane language

Not use false or misleading statements, or misrepresent themselves or any details of the debt they claim you owe

Avoid unfair practices, like charging unauthorized interest or fees

Stop contacting you if you request that they cease and desist

The Act mirrors the protections you have under the Fair Debt Collection Practices Act (FDCPA), which is federal law. If your rights are violated under the Rosenthal Act, you can submit a complaint to the California Attorney General. You could also sue the debt collector for damages caused by the violation.

Reviews and Testimonials from California

Very helpful

Desmond Zeigler, US

The light at the End of the tunnel. Dealing with financial struggles and trying to stay responsible with your lenders isn’t always easy—especially when life keeps happening. In my case, it was a cascade: a sick pet, rising insurance costs, unexpected car repairs, new tires, new glasses, and a partner who lost his source of income. I joined the program with several debts I had been working hard to pay off, but the high interest rates meant I was barely making a dent. After four months of pausing payments and redirecting that money into my dedicated account, I finally saw my first small debt settled. By the seventh month, one of my credit card companies accepted a negotiation. I’m now in the process of paying off that second card, while FDR continues to support me through two more ongoing negotiations. It’s a process—but one that’s giving me real hope. I’m so grateful for the help and support FDR has provided along the way. Thank you, FDR, for guiding me through to the light.

Neriza Lopez, US

Muy contento

Gabriel Navarro, US

California Debt Relief

Debt relief could help you shut the door on debt for less. Here's how debt settlement works.

You tell a debt expert about your debts.

Your debt expert looks at your budget to decide on a low monthly deposit you'll make while enrolled in the debt relief program.

That monthly deposit goes into a secure account.

The expert negotiates with creditors on your behalf.

Once your debt specialist reaches a settlement agreement with your creditor, you decide whether to approve it. If you give the green light, funds from your account are used to pay your creditor. Once you’ve satisfied the agreement, the rest of the debt is forgiven.

How do California debt settlement programs work, and what are their pros and cons?

California debt settlement programs negotiate with your creditors on your behalf. If your creditors agree, you pay them less than the full amount and they forgive the rest.

Most people enrolled in a debt settlement program choose to stop making debt payments so they can afford to save money for settlement offers. You put the money you would’ve used for monthly payments into a dedicated account for debt settlement. Once you’ve saved enough money, the debt settlement program can try to negotiate a lump-sum settlement for you. Some creditors agree to a series of payments, even with partial debt forgiveness.

Here are the pros and cons of California debt settlement programs.

Pros and Cons of California Debt Settlement Programs

| Pros | Cons |

|---|---|

| Could significantly reduce amount required to pay off your debt | Could hurt your credit score, although missed payments may have already damaged your credit |

| Might clear your debts faster than by making minimum payments | Creditors may attempt legal action |

| Streamline your monthly payments | Debt settlement isn’t guaranteed to work |

| Doesn’t require filing bankruptcy | Forgiven debt could be considered taxable income |

What is the typical duration and success rate of various debt relief programs available in California?

Here's what a typical debt relief plan in California looks like:

Average enrolled debt: $28,148

Average monthly program deposit: $461

Average monthly debt payment (pre-enrollment): $1,948

Average credit utilization before starting the program: 72.2%

With Freedom Debt Relief, you could get rid of your unsecured debt in as little as 24 to 48 months. And while you're in the program, you can rest assured there's a dedicated expert on your side to help you navigate the progress.

You might consider debt relief if you want to get out from under debt faster, mostly owe unsecured debts, and would like to reduce what you owe. If you're wondering whether debt relief is right for you, call 800-910-0065 to talk to a Freedom Debt Relief expert. They can evaluate your financial situation to help you decide whether debt relief is right for you.

Is Debt Consolidation the Best Debt Solution?

Debt consolidation is an alternative to debt settlement. When you consolidate debt, you take out a new loan and use the proceeds to pay off credit cards, medical bills, or other debts. That leaves you with one loan payment each month. You could also pay less in interest if your loan has a lower rate than the combined rate on your credit cards.

Is debt consolidation vs. debt settlement a better option? Yes, for some California residents, but not for everyone.

Debt consolidation could make sense if you:

Have good or excellent credit

Would like to simplify monthly debt payments

Owe an amount of debt you believe you can reasonably handle, since consolidation doesn't reduce the amount you owe. It only combines your debts.

Debt settlement may be the better choice if you:

Want to reduce the total amount you owe

Have experienced a financial hardship that makes it difficult to keep up with debt payments

Owe a larger amount of unsecured, high-interest debt

If you’re interested in debt consolidation, it's important to shop around. Compare personal loans for debt relief from different lenders to estimate how much you can borrow and what you'd pay in interest.

Differences between debt consolidation loans and debt management plans in California

Debt consolidation loans and debt management plans (DMPs) are strategies to manage debt.

A debt consolidation loan is a new loan that you use to pay off multiple existing debts. You might get a lower total monthly payment, a lower interest rate, or both.

To get a low interest rate, you need good credit. But even without good credit you might qualify for an interest rate that’s lower than the rate on your credit cards. Debt consolidation repayment terms usually last between two and six years.

A debt management plan is offered by credit counseling agencies. A counselor negotiates with creditors to reduce interest rates and create a structured repayment plan. You'll make a single monthly payment to the agency, which pays the creditors.

You don't need a specific credit score to get a DMP, but you may need to stop using your credit cards. You also need to be able to afford a payment designed to fully pay off your unsecured debts within three to five years.

List of accredited nonprofit credit counseling agencies in California offering debt management plans

Here are two places to find a list of accredited nonprofit credit counseling agencies in California:

The U.S. Department of Justice maintains a list of accredited nonprofit credit counseling agencies. You can filter the list by state to view credit counseling agencies that serve California.

The Department of Financial Protection and Innovation (DFPI) also has a page on credit counseling agencies. It includes a list of nonprofit credit counselors that have filed the documents to operate under California Financial Code section 12104.

Not all of these agencies may offer debt management plans. Services offered depend on the agency. Certain agencies focus specifically on courses for people planning to file for bankruptcy.

Another option is to use an organization that connects you with an agency based on your needs. Multiple organizations have networks of accredited credit counseling agencies. Options include the National Foundation for Credit Counseling (NFCC), Financial Counseling Association of America (FCAA), and American Consumer Credit Counseling (ACCC). Each organization has an online form you can submit to get connected with an agency.

Californians can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

What are the eligibility criteria for California state-sponsored debt relief programs?

California has a Debt Reduction Program for eligible parents paying child support. The program applies if you owe money to the state because your dependent children received public assistance or were in foster care while you weren’t paying court-ordered child support. You could reduce the debt you owe the state, but not to the person receiving the child support. Here’s how qualification works:

You must be able to pay any current child support payments and an ongoing debt payment.

Qualification depends on your income, assets, and cost of living. The size and makeup of your family are also important.

The general rule is that you might qualify if it’s unlikely you could pay off your debt to the state within 12 months.

Decisions are made on a case-by-case basis.

Los Angeles County has a Medical Debt Relief Program. To qualify, you must:

Be a current resident of Los Angeles County.

Earn no more than 400% of the federal poverty level or have medical bills that are 5% or more of your annual household income.

Have eligible medical debt.

Are there specific California government programs for student loan debt relief?

No. California doesn’t currently have any state-specific programs for student loan debt relief. There are some federal student loan forgiveness programs available. Federal student loans also provide the option of an income-driven repayment (IDR) plan for those who are eligible. An IDR plan could eventually lead to debt forgiveness after enough qualifying payments.

California also doesn’t offer debt relief for private student loans, nor are there any federal relief programs available for private loans. But private loans may be negotiable if you can’t make your payments. You could ask whether the lender offers loan forbearance or will accept a debt settlement. Here’s how each option works:

Forbearance is a temporary pause or reduction in your loan payments.

Debt settlement is when your creditor lets you close out the debt for less than what you owe.

If you want to settle your private student loans, you could negotiate yourself or work with a California debt relief company.

What options exist for medical debt relief for California residents?

Medical debt relief options for California residents include:

Financial assistance. Hospitals and healthcare providers may have financial assistance options available, such as discounted services or even debt forgiveness. Contact the healthcare provider, explain that you’re going through a financial hardship, and ask what your options are.

Debt settlement. If you can’t pay your bill in full, you could ask whether the healthcare provider will accept a smaller amount. Or a California debt settlement program could handle the negotiations on your behalf.

Government-sponsored medical debt relief. Los Angeles County’s Medical Debt Relief Program is one option. You could qualify for relief of eligible medical debt through this program if you’re a resident of Los Angeles County. The program requires that you earn less than or equal to 400% of the federal poverty level or that your medical bills are 5% or more of your annual household income.

How can you apply for the California Mortgage Relief Program?

The California Mortgage Relief Program offered assistance to homeowners whose homes were destroyed by natural disasters. As of November 2025, the program is no longer accepting applications.

A mortgage relief program is available to victims of the Los Angeles firestorms. Over 400 financial institutions have committed to the following mortgage relief:

90-day mortgage forbearance periods with a streamlined application process that doesn’t require forms or documents for requesting initial relief.

Lenders aren’t requiring immediate repayment of unpaid amounts at the end of the forbearance period.

Relief from mortgage-related late fees accrued during the forbearance period.

Protection from new foreclosures or evictions for at least 60 days.

No reporting of late payments for amounts in forbearance to credit agencies.

To get mortgage relief, you must be a qualified resident of Los Angeles County. You also need to be a customer of one of the institutions that has committed to offering mortgage relief. Contact your mortgage lender to request mortgage relief.

Even if you can’t get mortgage relief through this particular program, you can always contact your lender to find out what your options are.

What is the impact of enrolling in a California debt relief program on your credit score?

Enrollment in a California debt relief program doesn’t affect your credit score. But the debt relief process will likely have an impact on your credit.

People who sign up for debt relief programs usually choose to stop making payments on their debts. This serves two purposes:

It lets you save up money to offer your creditors to settle your debt

It sends a signal that you’re in financial distress. If you’re caught up on payments, a creditor might have a hard time believing that you can’t pay in full.

If you stop making your debt payments, your credit score is likely to drop. Payment history has the largest impact on your credit score. But if you’ve already fallen behind on your payments or have debt in collections, the damage might not be as bad as you expect. Your credit score has probably already taken a hit in that scenario.

In the long run, a debt relief program could put you in a better position to build and maintain a strong credit profile and better financial health. Debt relief helps you get rid of your debt. After that, you can focus on rebuilding your credit and designing a budget that helps you avoid crushing debt in the future.

Are there any California state grants available to help pay off personal debt?

No, there aren’t any California state grants to help pay off personal debt. But the state has many public assistance programs for households that meet income guidelines. If you qualify, you could apply for public assistance and put the money you save toward your debt.

Public assistance programs in California include:

CalFresh. Provides monthly food benefits to low-income individuals and families. The benefit amount depends on your income and monthly expenses.

CalWORKs. Provides cash aid and services to eligible California families in need. Families who qualify can receive money every month for housing, food, and other essential expenses.

Low-Income Home Energy Assistance Program (LIHEAP). Assists low-income households who pay a high portion of their income on their energy bill.

Cash Assistance Program for Immigrants (CAPI). Provides monthly cash benefits to aged, blind, and disabled non-citizens ineligible for Supplemental Security Income (SSI) or State Supplementary Payments (SSP) due to their immigration status.

Unemployment Benefits. Provide temporary income for eligible workers who lost their jobs or had their hours reduced through no fault of their own.

How can you identify legitimate debt relief companies in California and avoid common scams?

Here’s how to identify legitimate debt relief companies in California:

They don’t charge upfront fees. A common debt relief scam is an upfront fee. The Federal Trade Commission (FTC) has banned debt relief companies from doing this. Legitimate companies only charge a fee after they negotiate an agreement with your creditor, you approve it, and at least one payment is made.

They don’t contact you first. Quality debt relief companies don’t need to robocall people. They provide contact information and let you call if you need their services.

They don’t guarantee specific results. A debt relief company needs to negotiate with your creditors to figure out how much it can settle your debt for. An upfront guarantee to save you a certain amount on your debt is a red flag.

They have testimonials. If a debt relief company has made a positive impact in people’s lives, it should have testimonials from past clients. Look for a testimonials section, ideally with videos, for any debt relief company you’re considering.

What are the potential tax implications of debt forgiveness through California relief programs?

Both the IRS and the California Franchise Tax Board consider most forgiven debt to be taxable income. You may need to pay federal and state income taxes on debt forgiven during debt settlement or through another debt relief program.

Creditors are required to send you a Form 1099-C if they forgive $600 or more in debt. Unless you qualify for an exclusion, you would report your forgiven debt as "Other Income" on your annual tax return.

The most common exclusion for paying taxes on forgiven debt is insolvency—when you owe more than you own. You generally don't need to pay income taxes on forgiven debt if it's less than the amount you were insolvent at the time it was forgiven.

To determine insolvency, list out all of your assets, such as property, cash, and investments, and add up their values. Then, subtract any liabilities, including loans and credit card debt. If you get a negative amount, you are insolvent by that amount.

Can California debt relief programs assist with overwhelming payday loan debt?

Yes, California debt relief programs can help some people with payday loan debt. The right program will depend on how much debt you have and whether you can make monthly payments.

One option is credit counseling. A credit counselor can also set you up with a formal debt management plan (DMP). In this program, you make one monthly payment to the agency, which pays your creditors. A DMP can help you get lower interest rates on your debts but typically requires closing all your credit accounts. A DMP may also be able to get payday loan fees waived, and some credit counseling agencies may have stronger relationships with payday lenders than others.

Debt settlement is an option for people who can't afford to repay their payday loans in full. It involves negotiating with your creditors to accept less than you owe to get rid of your debts. You can try debt settlement yourself or hire a professional debt settlement company for a fee.

What are the alternatives to formal debt relief programs for individuals in California, such as DIY debt negotiation?

You can manage your own debt relief in California using a number of strategies. Most start with creating a personal budget.

A good budget should include all your income and expenses. It organizes your finances and shows you the extra money you could use toward debt repayment.

Then, pick a repayment strategy. In the debt snowball, make minimum payments toward all your debts, except the one with the lowest balance. Send all your extra cash to that one. Once that's paid, move on to the second-lowest balance, using the payment from your first paid-off balance. Your monthly payment snowballs with each paid-off debt. Knocking out debts can help you stay motivated.

Another option is the debt avalanche method, which puts any extra money toward the debt with the highest interest rate. This method lets you wipe out the most expensive debt first, so you pay less in interest overall.

DIY debt negotiation requires convincing your creditors to accept less than you owe to get rid of your debts. It takes persistence and organization to successfully negotiate debts.

Are there specialized debt relief options for seniors or veterans residing in California?

The California government doesn't have specific debt relief programs for seniors or veterans. However, the state government offers a variety of financial assistance programs that may help alleviate the burden of debt.

Seniors can contact the California Department of Aging (CDA) for information and resources for California residents. Veterans can contact the California Department of Veterans Affairs (CalVet).

California residents can also use a nonprofit credit counseling agency. Credit counselors can offer money management help as part of a debt management plan.

Debt consolidation is an option for people who can qualify for a new loan. You use the new loan to pay off multiple existing debts. The new loan should ideally have a lower interest rate than your current debt.

Debt settlement is another debt relief option in California. This involves negotiating with your creditors to accept less than you owe to get rid of your debts. You can handle debt settlement on your own or use a professional debt settlement company.

How do California’s community property laws affect debt liability and relief options for married couples?

California's community property laws mean that both people in a marriage equally own debts acquired while married—even if only one spouse signed for the debt. Debt that was taken on before the marriage is typically not part of community property.

Both spouses are equally responsible for repaying community debts. This means creditors and debt collectors can contact either of you in an attempt to collect payment. Any assets obtained during the marriage could also be subject to legal action.

While you're both responsible for community debts, you don't need to pursue debt relief jointly. You can use most debt relief strategies on your own, including credit counseling, consolidation, and debt settlement.

You can also file for bankruptcy individually or together with your spouse. Both options have pros and cons, depending on who owns the debt. A bankruptcy attorney can help you determine the best method for your specific situation.

What resources does the California Department of Financial Protection and Innovation (DFPI) offer for individuals seeking debt relief?

The DFPI doesn't offer debt relief programs, but California residents can find a lot of educational resources across several debt relief topics:

Consumer rights. This includes information on what debt collectors are allowed to do and how to avoid debt collection scams.

Find a credit counselor. The DFPI has a list of nonprofit consumer credit agencies that can offer debt management plans.

Your debt relief options. Learn the pros and cons of different debt relief options like debt settlement and consolidation.

You can also use the DFPI to verify businesses, like debt collectors, to ensure they’re licensed or registered with the state. This may help you avoid debt collection or debt relief scams from fraudulent companies.

If you think you’ve been the victim of a financial scam in California, you can file a complaint with the DFPI, in addition to the relevant federal agencies, such as the Federal Trade Commission. You can submit a DFPI complaint or inquiry online.

Are there any California debt relief programs specifically designed for small business owners facing financial hardship?

There are no programs specifically for small business debt relief in California. Several state programs have a mission of helping small businesses access capital for various needs, including:

California Small Business Loan Guarantee Program (administered by iBank)

California Capital Access Program (CalCAP)

Small businesses in California can also apply for federal Small Business Administration (SBA) loans if they qualify.

California small businesses can pursue other forms of debt relief, such as consolidation loans or debt settlement. Your business may also be eligible to file for bankruptcy.

Small business bankruptcy has two main types. If you want to try to save your business, you can file for Chapter 11 bankruptcy. You’ll still need to repay your debts, though you may be able to negotiate better repayment terms.

Chapter 7 bankruptcy is also known as liquidation and termination bankruptcy. Your business's assets will be sold to pay your creditors, and the rest of your unsecured business debt is typically discharged (forgiven). You then close your business down.

What are the legal consequences of defaulting on debt in California versus seeking a structured relief program?

You’re in default on a debt in California as soon as you stop making payments. While creditors can take legal action at this point, most will prefer less extreme collection efforts first. If those don't work, then your debt may be sold to a collection agency or you could be sued.

Creditors can take you to court over unpaid debts. If you lose the judgment, you could face garnishment of your paycheck. If you have secured loans, the collateral could be taken. In the case of a mortgage or auto loan, this would mean losing your house or vehicle.

You may avoid some of these legal consequences if you choose a structured debt relief program. For example, creditors can't sue you over debts that have been legally discharged in a bankruptcy.

Similarly, creditors may not need to take legal action if you enter into a debt management program (DMP) or have started negotiations as part of a debt settlement program.

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months